The global macroeconomic landscape is undergoing significant changes, with potential policy shifts such as broad tariff impositions under the Trump administration at the forefront. This analysis discusses the implications of such measures on global trade, interest rates, the U.S. dollar, and global growth, highlighting both challenges and opportunities in a volatile environment.

A Dynamic Decade: From Dull to Disruptive

The last few years have been markedly more interesting from a macro standpoint than the “dull” 2010-2020 decade of zero interest rates and quantitative easing. Looking ahead, it is evident that the macro landscape is poised for even greater transformation as macro catalysts abound from almost every angle. Yet, not all of these developments will be welcomed by markets: many expected geopolitical and macroeconomic policy shifts have the potential for being extremely disruptive while others can be very positive, for growth in particular. Crucially, most of these policy changes represent “tradable” events, where there are opportunities to forecast and structure trades around them.

One of the most impactful policies anticipated under Trump’s forthcoming administration is the broad imposition of tariffs on imports. Trump has consistently articulated his intention to significantly raise tariffs, a move which will undoubtedly have profound implications on international trade, currency valuations, monetary policy, and geopolitics. As his Cabinet takes shape, it becomes increasingly clear that Trump intends to deliver on these promises with tariffs likely exceeding expectations.

It is important to note that tariffs under Trump are not unprecedented. Under the previous Trump administration, the U.S. implemented five rounds of tariff increases on Chinese imports between July 2018 and September 2019, with China responding with its own retaliatory tariffs. In terms of magnitude, U.S. tariffs increased by approximately 20%, which was applied to just 17% of total U.S. imports. Since imports were roughly 15% of GDP, we can also represent this as a 20% tariff affecting 2.5% of GDP. However, the proposals being floated by both Trump and some of his key advisors now suggest a much larger scale, targeting a broader range of imports with significantly higher rates. The current proposal will apply to most imports, not only those coming from China, and the level will be much higher, close to 60% on China and 10%-20% on imports from other nations. This represents a marked escalation, roughly equating to a 20% tariff increase on 16% of GDP. This is about 7 times larger than the previous episode.

Implications of the Looming Tariff Escalation

The implications of these trade policies demand close attention. The theory of international trade is fascinating not the least because many results can be counterintuitive. For instance, the Lerner Paradox shows that under certain reasonable conditions, tariffs can deteriorate rather than improve the terms of trade on the imposing nation. These paradoxes highlight that trade measures trigger a broader set of reactions and counter-reactions, and simply analyzing the initial impact of a measure can be misleading. Hence, we need to consider both the direct and the indirect impact of the tariffs. Working under the assumption of a 60% tariff on China and a 15% tariff on the rest of the world:

Impact on Inflation and Federal Reserve Policy:During the 2018-2019 period, most tariff increases were passed on to consumers. Given the magnitude of the current proposals, foreign (non-U.S.) exporters and domestic (U.S.) importers might absorb some of the costs. However, a large share will undoubtedly pass on to consumers. If we do get a situation like 2018-2019, with an almost complete consumer pass through, core PCE could increase by as much as 1.2% (this includes the assumption that the U.S. dollar appreciates due to tariffs, otherwise the increase would be 1.5%). If such an increase materializes, we can see core PCE back to a 4% level. While tariffs are a one-off event (as the administration will not keep increasing them every year), we cannot fairly classify this episode as “inflation”. However, consumers do not discriminate between temporary or not; they simply perceive higher prices. The key here, and very relevant for the monetary policy response, is whether this increase influences inflation expectations. This brings a fascinating policy dynamic for the Federal Reserve. The Fed was badly burnt by the 2021-2022 fiasco of having characterized the massive surge in inflation as transitory. Will the Fed once again risk calling the surge in inflation transitory? Even if textbooks say that should be the case, the Fed might want to be pre-emptive and hike in the face of very elevated PCE.

Another fascinating aspect is in the realm of game-theory. If Powell is challenged by Trump not to increase rates, will Powell feel that he will lose all credibility if he does not hike, even if he thinks that the price impact is transitory? All in all, tariffs will represent a hawkish shock to U.S. interest rates with the Fed cutting much less than what is now priced in or even having to move back to hikes.

The U.S. Dollar: Short- and Long-Term Repercussions: Tariffs will have a direct and an indirect impact on the dollar, and both are bullish. Indirectly, the switch to a hawkish stance by the Fed is undoubtedly dollar positive. Furthermore, foreign central banks will face the opposite of what the Fed will face, i.e. deflationary dynamics coming from much weaker exports. All things equal, we should expect a move to a more dovish stance by these banks, adding further upward pressure to the U.S. dollar.

The direct effects are also dollar positive. The imposition of tariffs should have no effect on the balance of payments in the long run as the current account depends on the savings-investment relationship which is mostly unaffected by tariffs. The expected long-run adjustment to a tariff increase is an eventual reduction in exports along with imports that keeps the balance of payments unchanged. But in the short run (one-to-two-year horizon), there will be a reduction in domestic demand (U.S. based demand) for foreign currency as the U.S. will be importing fewer goods. This will push the dollar further up. All in, I expect a significant appreciation of the dollar if tariffs increase as expected.

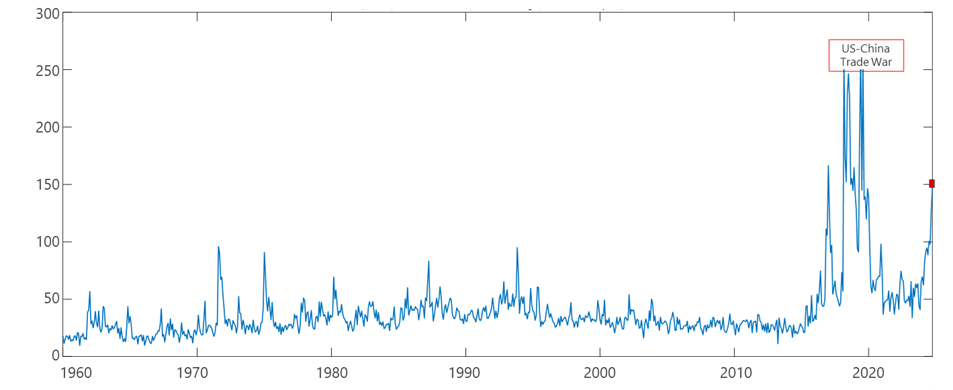

Global Growth Under Pressure:In the short run, U.S. growth might tick up, but more importantly the tariffs should be a negative impulse for global growth. China and Europe, already both in quasi-recessionary conditions, may be severely affected. Another dynamic aspect to consider is that of multiple retaliations. China retaliated each time that tariffs were imposed back in 2018-2019, and this can clearly happen again now. Furthermore, this trade war will heighten the already charged geopolitical environment. Tariffs do create a high degree of uncertainty (see graph below) beyond just trade uncertainty that should negatively weigh on growth, including the potential to weigh on U.S. growth. As the graph shows, we are already in a much more volatile environment, with this uncertainty likely to get worse before it gets better.

Trade Policy Uncertainty Index

Source: Dario Caldara, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo

Final Thoughts

The proposed tariff increases by the Trump administration represent a significant escalation with far-reaching consequences. From inflationary pressures and shifts in Federal Reserve policy to the potential global economic ripple effects, the implications are both profound and multifaceted. As far as the U.S. dollar is concerned, the combination of a more hawkish Fed and dovish foreign central banks, the diminished U.S. demand for foreign currency, and heightened geopolitics are all dollar positive. When one considers that other (non-trade related) potential policy measures of the new Trump administration, in particular fiscal and immigration policies, will also be dollar positive, it is a natural conclusion that we might face a new super-dollar era. As policymakers, investors, and businesses navigate these turbulent waters, a nuanced understanding of the interconnected macroeconomic dynamics will be essential. These “tradable” events underscore the importance of strategic foresight in leveraging opportunities while mitigating risks.

Author

Pablo Calderini

President and CIO

Pablo E. Calderini is the President and Chief Investment Officer of Graham Capital Management, L.P. (“Graham”) and is responsible for the management and oversight of the discretionary and systematic trading businesses at Graham. Mr. Calderini is also a member of the firm’s Executive, Investment, Risk, and Compliance committees. He joined Graham in August 2010. Prior to joining Graham, Mr. Calderini worked at Deutsche Bank from June 1997 to July 2010 where he managed several business platforms including Equity Proprietary Trading, Emerging Markets, and Credit Derivatives. Mr. Calderini received a B.A. in Economics from Universidad Nacional de Rosario in 1987 and a Masters in Economics from Universidad del CEMA in 1989, each in Argentina.

DISCLOSURE This presentation includes statements that may constitute forward-looking statements. These statements may be identified by words such as “expects,” “looks forward to,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “will,” “project” or words of similar meaning. In addition, our representatives may from time to time make oral forward-looking statements. Such statements are based on the current expectations and certain assumptions of Graham Capital Management’s (“Graham”) management, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Graham’s control, affect the operations, performance, business strategy and results of the accounts that it manages and could cause the actual results, performance, or achievements of such accounts to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical trends.

This document is not a private offering memorandum and does not constitute an offer to sell, nor is it a solicitation of an offer to buy, any security. The views expressed herein are exclusively those of the authors and do not necessarily represent the views of Graham Capital Management. The information contained herein is not intended to provide accounting, legal, or tax advice and should not be relied on for investment decision making.

Tables, charts, and commentary contained in this document have been prepared on a best-efforts basis by Graham using sources it believes to be reliable although it does not guarantee the accuracy of the information on account of possible errors or omissions in the constituent data or calculations. No part of this document may be divulged to any other person, distributed, resold and/or reproduced without the prior written permission of Graham.

Subscribe to our Resource Center

By clicking the Button you confirming that you’re agree with our following Terms and Conditions

By clicking register you are confirming that you agree with our following Terms and Conditions

Welcome to Graham Capital Management

By entering this website you are agreeing to its Terms of Use.

The risk of loss in trading commodities can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

In some cases, managed commodity accounts are subject to substantial charges for management and advisory fees. It may be necessary for those accounts that are subject to these charges to make substantial trading profits to avoid depletion or exhaustion of their assets. The disclosure document contains a complete description of the principal risk factors and each fee to be charged to your account by the commodity trading advisor (“CTA”). The regulations of the commodity futures trading commission (“CFTC”) require that prospective clients of a CTA receive a disclosure document when they are solicited to enter into an agreement whereby the CTA will direct or guide the client’s commodity interest trading and that certain risk factors be highlighted. This brief statement cannot disclose all of the risks and other significant aspects of the commodity markets. Therefore, eligible investors should carefully study the disclosure document to determine whether such trading is appropriate for you in light of your financial condition. Eligible investors are encouraged to access the disclosure document by contacting Graham, which will be provided at no additional cost. The CFTC has not passed upon the merits of participating in this trading program nor on the adequacy or accuracy of the disclosure document. Other disclosure statements are required to be provided to you before a commodity account may be opened for you. By accepting the terms of this statement and entering the site you are confirming your understanding of this statement.

Any “benefit plan investor” (e.g. An IRA or other ERISA investor) investor is hereby deemed to represent to Graham Capital Management (“Graham”) that an independent fiduciary (as defined in the ERISA fiduciary rule) is exercising its independent judgment with regard to such investor’s investment in any Graham managed fund and is aware of and acknowledges and agrees that Graham and its affiliates are relying on the exception set forth in clause (c)(1) of the ERISA fiduciary rule (i.e., the “transactions with independent fiduciaries with financial expertise” exception) with respect to any communications made to the investor or the investor’s fiduciary that are considered recommendations concerning any transaction and such benefit plan investor.

Although the site may include investment-related information, nothing on the site is a recommendation that you purchase, sell or hold any security or other investment, or that you pursue any investment style or strategy.

We do not give any advice or make any representations through the site as to whether any investment is suitable to you or will be profitable.

Nothing on the site is intended to be, and you should not consider anything on the site to be, investment, accounting, tax or legal advice. If you would like investment, accounting, tax or legal advice, you should consult with your own financial advisors, accountants or attorneys regarding your individual circumstances and needs.

The past performance of any investment, investment strategy or investment style is not indicative of future performance.

If you have been provided with a password to access the site you are solely responsible for maintaining the confidentiality and security of your password. You may not disclose your password to any third party. You accept full responsibility for any use of your password. You must notify Graham immediately of any actual or suspected loss, theft or unauthorized use of your password.

We are not obligated to inquire as to the authority or propriety of any use of or action taken under your password. We will not be responsible for any loss to you that arises from such use or action or from your failure to comply with these provisions.

The site, including all content, is provided as is and as available.

We disclaim all representations and warranties, express or implied, of any kind with respect to the site and the content including warranties of merchantability, fitness for a particular purpose and non-infringement of intellectual property and proprietary rights.

Without limiting our general disclaimer, we do not warrant the availability, accuracy, completeness, timeliness, functionality, reliability, sequencing or speed of delivery of the site or the content.