As uncertainty reigns in today’s macroeconomic environment, investors must balance caution with opportunity.

August’s Volatility Shock

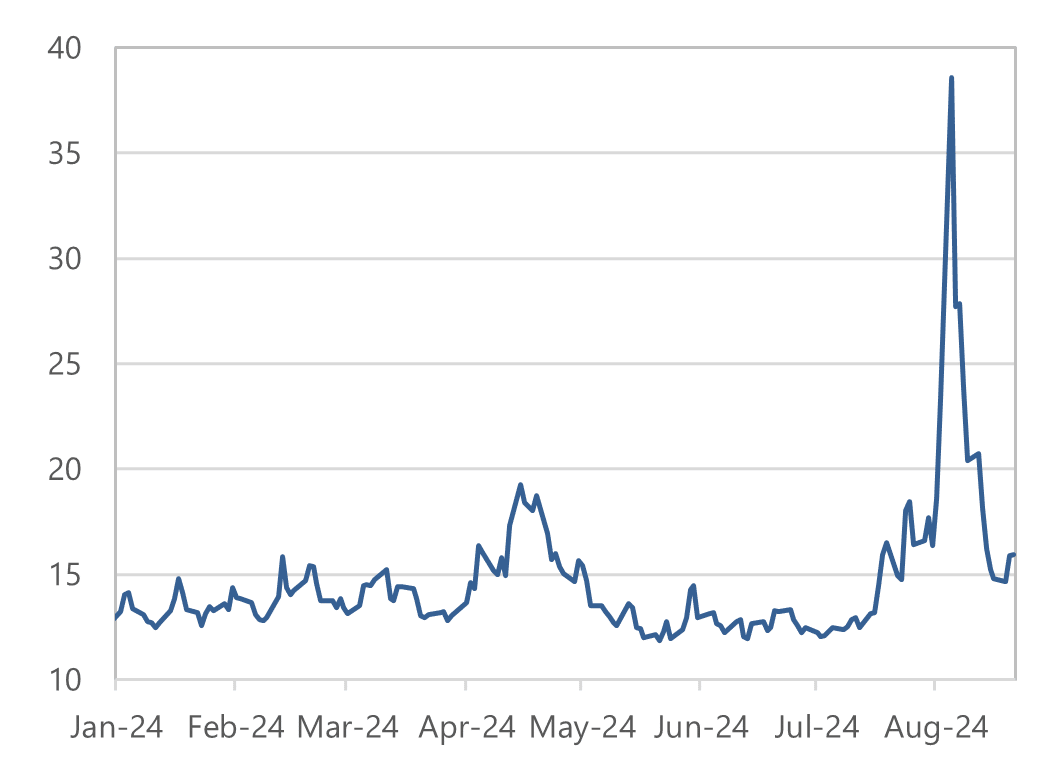

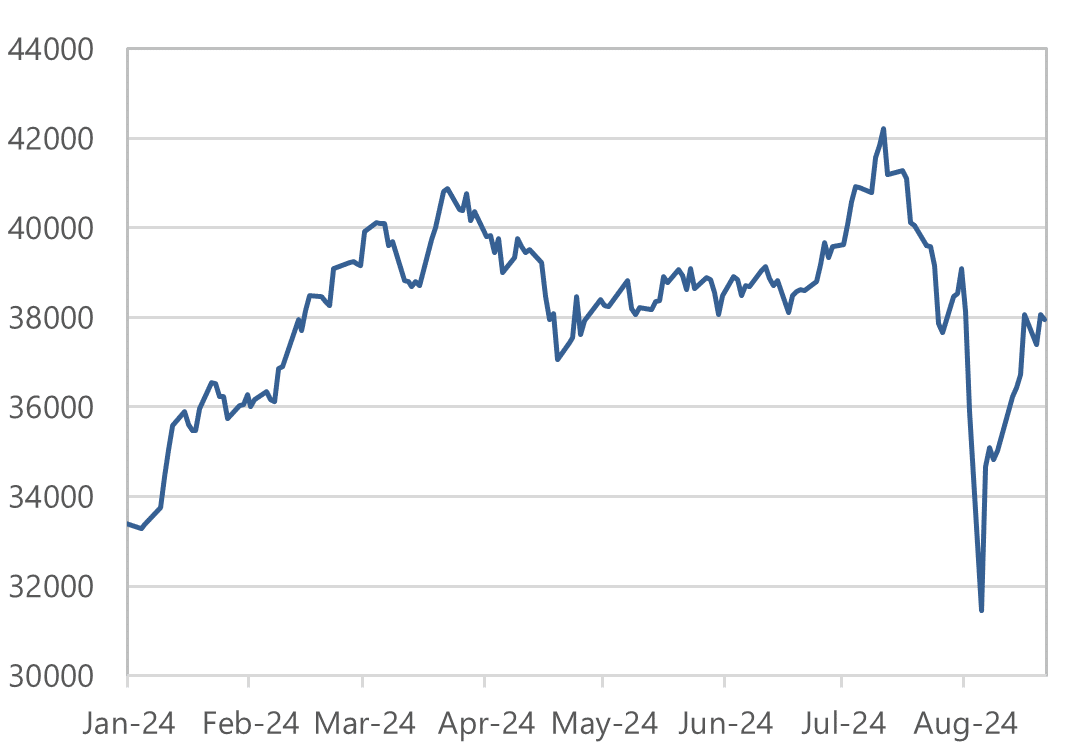

August began with one of the most virulent and unanticipated spikes in implied volatility on record. Equally remarkable was the speed of normalization in volatility. On August 1, the VIX traded around 16% and within two business days it spiked to a high of 67% to then fall to around 22% by August 7. For some markets, particularly Japanese equities, this was the sharpest sell-off in memory. At its worst, the Nikkei plummeted more than 20% within a three-day period, which implies a 20 sigma move. Under a normal distribution the probability of observing such event is an astronomically low 5.5e-89 (in English, 5.5 divided by a number with 89 zeros!). While returns are not Gaussian, these moves are extreme by any standard.

COBE VIX Index

Nikkei Index

Currencies also experienced significant volatility, especially currency pairs heavily included in carry trades. The sell-off was extraordinary not only given the speed of both the sell-off and very quick recovery but also due to the lack of catalysts. To be certain, there were a few shocks in the preceding week (perhaps most notably, the BOJ rate hike) but there was no real proportionality between the magnitude of the shocks and the extreme market response. All in all, this was a massive deleveraging shock more than anything else. While it may be premature to assume all things are back to normal, markets appear to be in much better shape as leverage has been substantially reduced.

Global Economic Growth, Inflation, and Labor Market Trends

As we move into the second half of the year, the U.S. economy continues to march along a path of “moderated resilience.” Current GDP forecasts are around 2.2% for 2024 and 2% for both 2025 and 2026. These GDP readings, being so close to the 1.8% steady-state equilibrium level and having such low standard deviation (they all cluster around 2.2%), have generally created a favorable backdrop for equities and risk assets so far this year. Furthermore, we have seen a big reversal of the inflationary resurgence that we saw in Q1, with core PCE inflation moderating from a 4.5% 3-month annualized rate at the end of March to a 2.3% 3-month annualized rate by June.

However, the labor market data has shown a very rapid deterioration of late. The ISM Employment Index dropped 5.9 points in July to 43.4, which is the lowest level for this index since June 2020. The Employment data for July also showed weakness across the board. The concern is that rapidly deteriorating labor markets tend to perpetuate their own decline. Historically recessions usually start with a gradual worsening of labor markets, which then accelerates as weaker labor conditions trigger reductions in aggregate demand conditions, leading companies to further layoffs.

Outside the U.S., things are not favorable from a macroeconomic standpoint. Europe, particularly Germany, is still suffering from the consequences of the Russia-Ukraine war as well as the continued sluggishness in China. German GDP is in negative territory after several years of anemic growth. Furthermore, the European industrial complex is very heavy on machine tools and luxury goods and significantly lags behind the U.S. in technology and AI.

Major emerging market economies are also lagging due to a combination of a Chinese sluggishness, the Russia-Ukraine war, a strong U.S. dollar and, more importantly, the fact that sticky U.S. inflation has not allowed the Fed to cut, so several of the main emerging market central banks have had to keep their policy rates at extremely high levels to avoid excess currency depreciation. For example, the policy rate in Brazil (SELIC) is at 10.5% versus annual core inflation at 3.5%, while for Mexico the Banxico policy rate is at 11% versus core CPI with a 4% handle. These are extremely high real rates even by EM standards.

Monetary and Fiscal Policy Outlook

Beginning with the Fed, against the backdrop of gradually moderating inflation and low but rapidly deteriorating unemployment, it is expected that the Fed will deliver its first rate cut at the September meeting. The Fed has also signaled its intention to ease preemptively to preclude any undesired slowing in growth and labor markets, and as the economy is entering the easing cycle in a relatively resilient place. The economic backdrop has been so far most analogous to the Fed’s 1995 easing cycle when they similarly approached the inflation target from above but were concerned about downside risks to growth. In that cycle, the Fed only delivered 75bps of total easing, holding steady after they assessed the risks had become more balanced. If they embark on a similar trajectory this cycle, barring an exogenous shock to the economy, the base case is that the Fed follows its implied Summary of Economic Projections (“SEP”) plan in delivering these 75bps of cuts quarterly. However, the Fed will cut faster and more aggressively if the labor market continues to deteriorate at the pace it showed in July.

The ECB, after delivering their first rate cut in June, held steady in July and centered any future easing around quarterly forecast meetings, contingent on inflation tracking towards their end-2025 target. The most likely scenario is that the ECB cuts another 50bps by year-end for a total of 75bps cuts this year.

In the U.S., from a fiscal standpoint, while the deficit has narrowed by about 15% compared to last year, it remains at an exceptionally high level despite fairly high nominal GDP growth. The concern is that a significant slowdown in growth could reduce tax revenues and increase government spending due to rising unemployment, potentially pushing the deficit close to double digits once again. Interestingly, neither presidential candidate appears committed to any serious fiscal reform, leaving little hope that the fiscal accounts will improve in the next few years.

Geopolitical Influences on Market Dynamics

On top of the many interesting macroeconomic dynamics at play, we are currently facing a highly charged geopolitical landscape. Recent elections in Mexico, South Africa, the UK, and France, just to name a few, and the upcoming U.S. presidential election are starting to weigh heavily on market dynamics. In the U.S., markets are starting to move based on the so-called “Trump and Harris trades,” referring to potential market strategies based on the policies of the respective presidential candidates. So far, Harris has not been forthcoming about how she will deviate from the current administration’s policies, so the Harris trades have more to do with keeping the status quo. Likely, and based on her track record as a Senator, Harris’ policies will be to the left of the current ones. However, without an explicit agenda put forward, the market will not be too keen to underwrite anything more than the continuation of the current set up. In contrast, a Trump administration can bring significant changes to tax, trade, regulatory, and immigration policies. To date, both Trump and his running mate J.D. Vance have been very explicit about the need for deep reforms. The most relevant policies from a macro standpoint can be summarized as:

Tariff increase, at least 10% across the board and likely as high as 60% for Chinese goods

Immigration reform/deportations that can see several million workers leave the workforce

De-regulation that can significantly boost investment

The one clear thread of all these policies is that they will push inflation back up, potentially by several hundred basis points, at least in the short-term. A key question is how the Fed will react to this potential development. I can think of two critical decisions that the Fed will face if Trump wins the election. First, if the economy slows down significantly towards the end of 2024, would the Fed cut more than what is priced knowing that they might need to hike again in 2025? Secondly, will the Fed see these price increases as transitory and hence not “inflationary,” or will they be concerned about inflation expectations moving back up and bring Fed funds significantly up to combat inflation? I want to make clear that we are not assuming a Trump win. As we stand the election is very close to even but then this means that there is 50% probability of a Trump presidency and hence the markets have to somehow price Trump’s policies by that much.

On top of these political aspects, there are many international geopolitical hot spots that can potentially be major market movers. To begin, we are witnessing an escalation of the Middle East conflict. Israel currently faces at least two major conflicts, one with Hamas and another with Iran/Hezbollah. Either one of these conflicts, particularly the Iran/Hezbollah conflict, has the potential to escalate significantly. In Asia, unbeknownst to many, the Philippines and China are playing a very risky game of war where a small mistake can trigger a full-blown armed conflict between them. The key issue here is the mutual defense treaty between the United States and the Philippines that requires the U.S. to defend the Philippines from a Chinese attack and hence the potential for this regional conflict to escalate into a major global conflict. In such a heightened geopolitical environment, it is crucial to be aware of all these events and have ex-ante road maps of what can happen and how markets can react. While these are probabilistic assessments, understanding potential left tail scenarios is valuable. It can help position the portfolio in a specific direction or at least protect it from extreme events.

Market Implications of Recent Macro Developments

The combination of stable, near-equilibrium growth, moderating inflation, and anticipated Fed rate cuts has certainly been a good setup for equities so far (even when we consider the extreme volatility of the first week of August). However, the rapidly deteriorating labor data and the idea that the Fed will be late to cut like they were late to hike is making markets very uneasy and pushing volatility up to levels not seen in months. But even before the weak July labor data, the market was already showing some cracks beneath the surface. For example, there has been massive volatility across sector and factor returns. Even before the extreme events of August, we saw a record rotation from large-cap tech to small caps, with the Russell 2000 outperforming the Nasdaq by nearly 20% over a two-week period at the end of July. However, about 30% of this outperformance was reversed in just three days at the beginning of August. Until recently, very low VIX levels did not reflect the much higher single-stock volatility we were experiencing, which was instead due to extremely low correlations between individual stocks. Similarly, the VIX has shown extreme fragility, with levels doubling in the last two weeks having also reached record highs in the first few days of August.

We are certainly in a very rapidly changing environment, and it is important in this context to follow the data but also market technicals very closely. On the one hand the economy is still strong and corporate earnings have so far shown resilience with 80% of S&P companies beating expectations to date for Q2. On the other hand, markets are overextended and are likely to react with sell-offs if the data continues to weaken, especially with the next Fed meeting not scheduled until September 18.

In rates, there has been a very significant repricing of Fed expectations with markets now pricing 110bps of cuts to December. However, these dynamics are partly technical and reflecting a risk-off induced rates rally. Clearly, if the labor market data continues to weaken at the pace it showed in July, the Fed will need to cut rates more significantly than what the market is currently pricing. However, looking ahead and assuming some labor market stability, we face the crosscurrents between current tight monetary policy plus a slowing economy versus the potential for significant inflationary pressure under a Trump administration. It is clear that the combination of tax cuts, tariffs, and a reduced labor force can have a significant impact on inflation. Regardless of the scenario, it seems likely that the yield curve will steepen. First, due to the large deficits, we will continue to have record Treasury auctions for years to come, which will put pressure on the long end. Then, if there is a resurgence in inflation, the Fed might hike. However, with policy rates already so restrictive, they might not hike as much as it is needed to rein in inflation and hence the curve will bear steepen. Conversely, the curve can bull steepen as the Fed cuts rates if Harris wins or if Trump is not able or willing to implement his full agenda.

I think the U.S. dollar, perhaps with the exception of dollar-yen, will recover from the recent losses and continue to push higher. While the U.S. dollar is actually very expensive and close to a record valuation on a trade-weighted basis, at the same time, the combination of anemic growth for the rest of the world together with the high USD carry creates strong support for the dollar. In the past, we have seen how at the onset of easing cycles the U.S. dollar can weaken as the Fed tends to lead the cycle, but this dynamic can quickly reverse when it becomes evident that global central banks will follow the Fed and cut rates as well. On top of that, the U.S. dollar is a great hedge for both potential equity weakness and geopolitical shocks. It is relevant to highlight once again that Trump policies are very much dollar positive despite his rhetoric of wanting a cheap dollar. One last word about this issue, currencies strongly follow current and expected monetary policy first, trade policy second, and then geopolitical events. Treasury has little control on any of these variables outside from trade where Trump has committed to higher tariffs, which will make the dollar stronger not weaker, in particular against CNY.

A Complex but Opportunity-Rich Environment

It is difficult to remember a time that was so interesting in the macro environment. The current economic landscape is characterized by a mix of moderated growth, easing inflation, and complex geopolitical factors. While the outlook for equities remains positive, supported by anticipated monetary easing and a strong U.S. dollar, potential risks from labor market vulnerabilities and global macroeconomic uncertainties cannot be ignored. Investors must navigate these dynamics carefully, balancing optimism with caution, as the economic and policy environments evolve. The intersection of these factors creates a challenging yet opportunity-rich environment, demanding strategic foresight and adaptability in investment approaches.

Author

Pablo Calderini

President and CIO

Pablo E. Calderini is the President and Chief Investment Officer of Graham Capital Management, L.P. (“Graham”) and is responsible for the management and oversight of the discretionary and systematic trading businesses at Graham. Mr. Calderini is also a member of the firm’s Executive, Investment, Risk, and Compliance committees. He joined Graham in August 2010. Prior to joining Graham, Mr. Calderini worked at Deutsche Bank from June 1997 to July 2010 where he managed several business platforms including Equity Proprietary Trading, Emerging Markets, and Credit Derivatives. Mr. Calderini received a B.A. in Economics from Universidad Nacional de Rosario in 1987 and a Masters in Economics from Universidad del CEMA in 1989, each in Argentina.

DISCOSURE

This presentation includes statements that may constitute forward-looking statements. These statements may be identified by words such as “expects,” “looks forward to,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “will,” “project” or words of similar meaning. In addition, our representatives may from time to time make oral forward-looking statements. Such statements are based on the current expectations and certain assumptions of Graham Capital Management’s (“Graham”) management, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Graham’s control, affect the operations, performance, business strategy and results of the accounts that it manages and could cause the actual results, performance, or achievements of such accounts to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical trends.

This document is not a private offering memorandum and does not constitute an offer to sell, nor is it a solicitation of an offer to buy, any security. The views expressed herein are exclusively those of the authors and do not necessarily represent the views of Graham Capital Management. The information contained herein is not intended to provide accounting, legal, or tax advice and should not be relied on for investment decision making.

Tables, charts, and commentary contained in this document have been prepared on a best-efforts basis by Graham using sources it believes to be reliable although it does not guarantee the accuracy of the information on account of possible errors or omissions in the constituent data or calculations. No part of this document may be divulged to any other person, distributed, resold and/or reproduced without the prior written permission of Graham.

Subscribe to our Resource Center

By clicking the Button you confirming that you’re agree with our following Terms and Conditions

By clicking register you are confirming that you agree with our following Terms and Conditions

Welcome to Graham Capital Management

By entering this website you are agreeing to its Terms of Use.

The risk of loss in trading commodities can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

In some cases, managed commodity accounts are subject to substantial charges for management and advisory fees. It may be necessary for those accounts that are subject to these charges to make substantial trading profits to avoid depletion or exhaustion of their assets. The disclosure document contains a complete description of the principal risk factors and each fee to be charged to your account by the commodity trading advisor (“CTA”). The regulations of the commodity futures trading commission (“CFTC”) require that prospective clients of a CTA receive a disclosure document when they are solicited to enter into an agreement whereby the CTA will direct or guide the client’s commodity interest trading and that certain risk factors be highlighted. This brief statement cannot disclose all of the risks and other significant aspects of the commodity markets. Therefore, eligible investors should carefully study the disclosure document to determine whether such trading is appropriate for you in light of your financial condition. Eligible investors are encouraged to access the disclosure document by contacting Graham, which will be provided at no additional cost. The CFTC has not passed upon the merits of participating in this trading program nor on the adequacy or accuracy of the disclosure document. Other disclosure statements are required to be provided to you before a commodity account may be opened for you. By accepting the terms of this statement and entering the site you are confirming your understanding of this statement.

Any “benefit plan investor” (e.g. An IRA or other ERISA investor) investor is hereby deemed to represent to Graham Capital Management (“Graham”) that an independent fiduciary (as defined in the ERISA fiduciary rule) is exercising its independent judgment with regard to such investor’s investment in any Graham managed fund and is aware of and acknowledges and agrees that Graham and its affiliates are relying on the exception set forth in clause (c)(1) of the ERISA fiduciary rule (i.e., the “transactions with independent fiduciaries with financial expertise” exception) with respect to any communications made to the investor or the investor’s fiduciary that are considered recommendations concerning any transaction and such benefit plan investor.

Although the site may include investment-related information, nothing on the site is a recommendation that you purchase, sell or hold any security or other investment, or that you pursue any investment style or strategy.

We do not give any advice or make any representations through the site as to whether any investment is suitable to you or will be profitable.

Nothing on the site is intended to be, and you should not consider anything on the site to be, investment, accounting, tax or legal advice. If you would like investment, accounting, tax or legal advice, you should consult with your own financial advisors, accountants or attorneys regarding your individual circumstances and needs.

The past performance of any investment, investment strategy or investment style is not indicative of future performance.

If you have been provided with a password to access the site you are solely responsible for maintaining the confidentiality and security of your password. You may not disclose your password to any third party. You accept full responsibility for any use of your password. You must notify Graham immediately of any actual or suspected loss, theft or unauthorized use of your password.

We are not obligated to inquire as to the authority or propriety of any use of or action taken under your password. We will not be responsible for any loss to you that arises from such use or action or from your failure to comply with these provisions.

The site, including all content, is provided as is and as available.

We disclaim all representations and warranties, express or implied, of any kind with respect to the site and the content including warranties of merchantability, fitness for a particular purpose and non-infringement of intellectual property and proprietary rights.

Without limiting our general disclaimer, we do not warrant the availability, accuracy, completeness, timeliness, functionality, reliability, sequencing or speed of delivery of the site or the content.