The U.S. tariff overhaul marks a historic policy rupture with profound implications for global markets and macroeconomic stability—ushering in an era where uncertainty is the dominant risk factor. In this new paradigm, agility and active risk management are essential for generating alpha.

A Paradigm Shift in Policy and Markets

On April 2, 2025, “Liberation Day” marked a turning point for markets—one defined by sharp volatility, deepening investor anxiety, and the realization that traditional policy guardrails may no longer apply. Investors were forced to confront the real-world implications of President Trump’s tariff policy. In the span of 48 hours, a policy shock transformed into a global market event. China responded almost immediately with retaliatory measures, and what followed was a sharp repricing of risk across asset classes, reflecting fears of a negative-feedback loop that could tip the global economy into recession. Since then, the administration has announced a three-month delay in implementing the “reciprocal” rate structure, while going ahead with the baseline 10% tariff for most countries—though certain sector-specific tariffs remain. However, the trade confrontation with China continued to escalate, confirming market fears that a broad trade war between these two largest economies is now fully underway.

The numbers underscore the scale of the market’s reassessment. The S&P 500 fell 9% on the week, erasing over $5 trillion in market capitalization. The Nasdaq 100 entered a bear market. Volatility surged, with the VIX spiking to 45—the highest since the COVID crisis in 2020—and traditional safe havens initially rallied, with U.S. Treasuries and the Japanese yen both catching strong bids. Later on, however, even Treasury markets showed significant stress, with U.S. yields rising while other risk assets sold off. Oil and copper sold off sharply, while credit markets showed early signs of stress, with spreads widening at the fastest pace since the 2023 regional banking turmoil.

Even solid economic data was brushed aside. A stronger-than-expected U.S. payrolls report failed to shift sentiment, as investors quickly pivoted to focus on forward-looking risks. In the view of our economists, the probability of a shallow recession has risen materially, even though the tail risk of a deep economic contraction was reduced after the three-month delay of a possible extreme tariff shock.

In our view, the policy changes by the Trump administration are not a cyclical adjustment—it is a structural pivot, with the global economy facing its most dramatic macroeconomic and geopolitical realignment since the 1930s. A policy shift of these historic proportions has the potential to unravel the system that the United States spent decades building in the aftermath of World War II. This is not merely a shift in trade policy; it’s a dismantling of the global economic order with wide ranging implications.

Uncertainty is the Risk

Perhaps as unsettling as the scale is the ambiguity: The stated rationale behind the tariff policy—aimed at correcting trade imbalances—deviates from conventional economic orthodoxy, instead reflecting a protectionist approach in which trade deficits are equated with economic vulnerability. The back-and-forth around key policies and abrupt reversals—such as the recent delay of the reciprocal tariff structure—make it difficult for companies and investors to adjust with confidence, as the future policy landscape remains highly uncertain. As markets reeled, the absence of a clear response from policymakers only compounded the uncertainty.

For equity investors, the current moment is particularly challenging. The binary nature of the policy outlook—where tariffs could be reversed or become entrenched—creates a dilemma. Panic selling risks missing a rapid rebound, while holding on assumes a rational resolution that has yet to materialize. As we’ve seen from the market whiplash in the first two weeks of April, the result is a risk environment that is structurally asymmetric and tactically unpredictable.

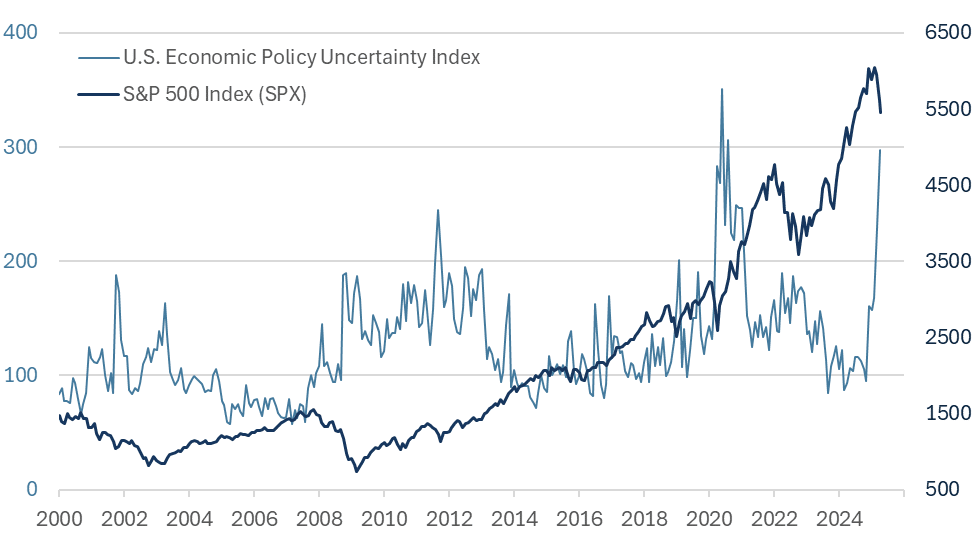

More broadly, the market is grappling less with the first-order impacts of tariffs—which will take time to work through—and more with the corrosive effects of sustained uncertainty. And yet, as the chart below shows, despite a surge in the U.S. Economic Policy Uncertainty Index to levels last seen during the pandemic—and a clear deterioration in sentiment and risk appetite in Q1 2025—the correction in equity markets has only been modest given the previous run up in valuations. Even though the recent sell-off suggests elevated uncertainty should be “priced in,” equities remain expensive by most historical measures.

Risk and Uncertainty

Data Source: Bloomberg and Economic Policy Uncertainty

The economic uncertainty is now more damaging in the near term than the tariffs themselves, which will take time to fully impact supply chains and corporate margins. Without a clear sense of the U.S. administration’s endgame—or even whether one exists—investors are left to navigate a landscape defined less by data, and more by the absence of a coherent framework.

The Fed’s Bind

The Federal Reserve faces an increasingly difficult path forward. With the high inflation from 2022 still fresh in their memory, the Fed will be reluctant to call inflation “transitory” again and move quickly to cut rates, even as recession risks rise. The administration’s quick policy reversals may also stay their hand, as they will not want to preemptively cut rates, only to realize that the policy outlook has shifted again. But should the tariffs persist and the economy soften materially, the policy response may need to be deeper and more prolonged than markets currently anticipate. This dynamic—where cuts are delayed but ultimately more aggressive—could create opportunities in the middle of the yield curve.

Beyond the U.S., central banks globally are navigating similarly fraught territory. The economic spillovers from U.S. tariffs will vary depending on direct exposure, retaliatory measures, fiscal space, and currency resilience. However, the broader picture is one of rising global downside risk. Weaker U.S. growth and softening demand in China could tip the global economy into a synchronized downturn—especially impacting small, open economies like the UK and Australia, where the direct tariff hit may be modest, but the second-order effects could be severe.

Monetary authorities in these regions are taking note. The Bank of England, Bank of Canada, and Reserve Bank of Australia have all struck a more cautious tone, acknowledging the stagflationary threat posed by global trade tensions. As BoC Governor Tiff Macklem noted, “monetary policy cannot offset the impacts of a trade war.” Even so, the market continues to price in a series of rate cuts through year-end—three each from the BoC and RBA, and up to five from the BoE—as these central banks move policy to their neutral estimates. Still, with inflation risks lingering, the room to cut deeply into accommodative territory remains limited.

As a result, policy responses will be uneven, sentiment-driven, and often behind the curve. For investors, the interplay between policy constraints and global fragility demands a high degree of vigilance and tactical flexibility.

Global Dominoes

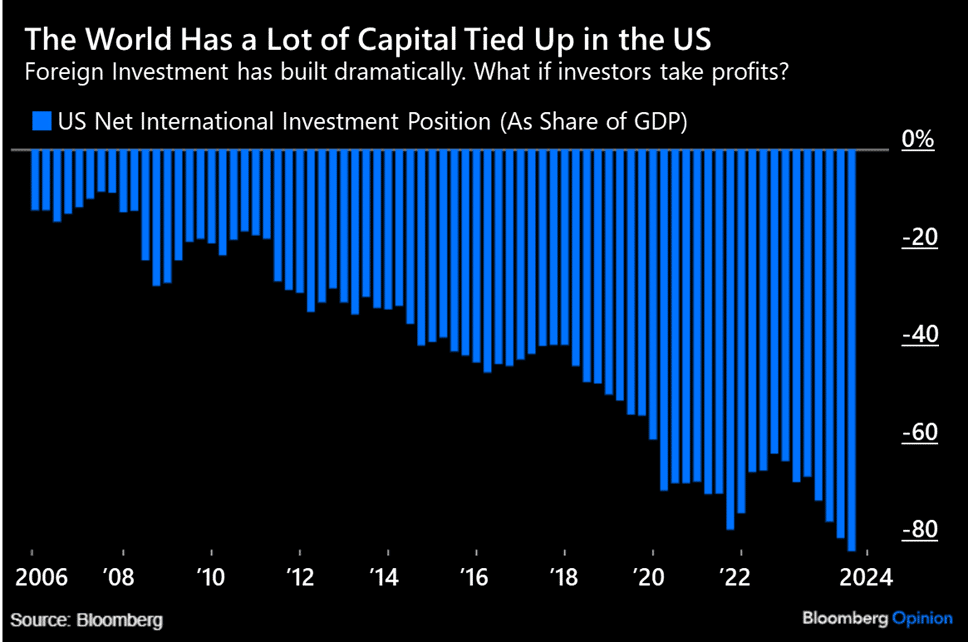

The international response to U.S. tariffs will be critical, not only in terms of retaliation, but also in how it reshapes global capital flows and economic alignments. If higher barriers to trade result in the U.S. importing less, other countries will accumulate fewer dollars—limiting their ability to reinvest in U.S. assets. As countries like Germany move toward greater defense autonomy and infrastructure investment, they will likely need to retain more capital domestically to support rising debt issuance. This would mark a sharp reversal from a multi-decade trend of global capital chasing U.S. yield and safety.

Historically, strong foreign demand for U.S. assets has supported a premium in American markets, even as the U.S. has taken an outsized share of global capital relative to its contribution to earnings. But signs of that premium beginning to unwind have already begun to emerge, raising important questions about the sustainability of current capital flows. What if the policies designed to shrink trade deficits also shrink the very capital inflows that finance them? It remains unclear whether the administration is weighing this risk—balancing tariff revenue against the potential for higher funding costs and reduced global demand for U.S. financial assets.

Foreign Investment in the U.S.

In parallel, traditional safe havens are seeing renewed interest. Gold continues to trade as a consensus hedge, though positioning is increasingly crowded and vulnerable to sentiment shifts. The Japanese yen, by contrast, remains in our view fundamentally undervalued and stands out as one of the few assets that offer both defensive characteristics and valuation support.

Funding Market Stress and the “Trump Put”

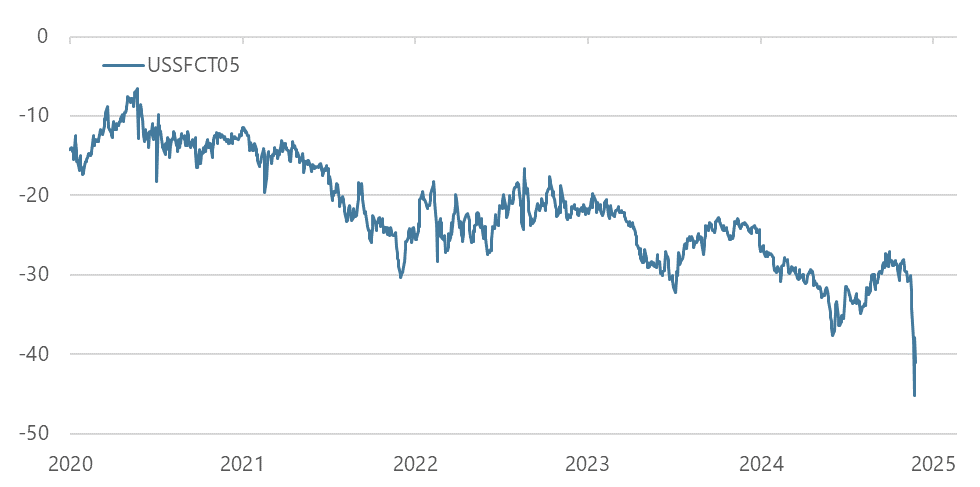

While risk assets have faced pressure from tariffs and geopolitical volatility, a less visible but equally important shift has emerged in funding markets. The U.S. Treasury market experienced a sharp selloff, with 10-year yields surging by 17 basis points in a single day on April 7th—the most significant intraday move in two decades and unusual as it occurred during a sell-off in equity and credit markets. U.S. Treasuries failed to provide protection. The forced selling and emerging liquidity pressures echo the dynamics of March 2020, when market functioning deteriorated sharply amid unwinds of highly levered basis positions—ultimately prompting the Federal Reserve to intervene with $1.6 trillion in Treasury purchases to restore stability. Swap spreads have moved sharply, indicating tightening liquidity conditions. Similar to March 2020, the post-GFC regulation has a pro-cyclical impact on funding markets: at the same time as market participants are rushing for cash, banks tightened liquidity and add to the stress. The liquidity provider of last resort is the Fed and rumors about a possible intervention emerged. While it appears to us that the administration is more tolerant to equity sell-offs than previously assumed, it has shown greater sensitivity when stress emerges in the plumbing of financial markets. Just days after rolling out the “reciprocal” tariff structure, President Trump unexpectedly announced a 90-day pause—a potential response not to falling stock prices, but to growing dysfunction in funding markets. The ‘Trump put’ may still be in play, but its strike may be in the costs of funding levels, not that of the S&P 500.

Swap Spreads Signal Stress

Data Source: Bloomberg

Final Thoughts: Positioning Through Complexity

Even after the recent sell-off, markets remain broadly expensive, particularly within U.S. equities, where valuations continue to reflect optimism that may not be aligned with rising macro and policy uncertainty. Credit markets also appear stretched, with spreads—particularly high yield spreads—only recently beginning to price in the potential for a broader economic slowdown or policy missteps. In this context, our portfolio managers remain sharply focused on managing exposures and avoiding areas of concentrated tail risk.

In the current environment, our focus is to prudently manage risk and maintain a flexible, tactical approach. While elevated uncertainty has naturally tempered our conviction and therefore our risk-taking, we remain prepared to act when high-conviction opportunities emerge. Market dislocations will create openings, but capitalizing on them will require careful attention to portfolio construction, timing, and sentiment. This is not a backdrop that favors sweeping macro views or static positioning. Rather, it calls for adaptability, thoughtful execution, and a willingness to reassess as conditions evolve.

Our mandate remains unchanged: to deliver alpha, especially in challenging market environments. That means preserving capital, managing risk with discipline, and being ready to act decisively when the opportunity set warrants it. We draw confidence from our experience and our process, built over three decades of navigating complex market cycles. And in today’s landscape, confidence must be paired with humility—because certainty, increasingly, is in short supply.

Author Pablo Calderini Vice Chairman and Co-CIO

Pablo E. Calderini is the President and Chief Investment Officer of Graham Capital Management, L.P. (“Graham”) and is responsible for the management and oversight of the discretionary and systematic trading businesses at Graham. Mr. Calderini is also a member of the firm’s Executive, Investment, Risk, and Compliance committees. He joined Graham in August 2010. Prior to joining Graham, Mr. Calderini worked at Deutsche Bank from June 1997 to July 2010 where he managed several business platforms including Equity Proprietary Trading, Emerging Markets, and Credit Derivatives. Mr. Calderini received a B.A. in Economics from Universidad Nacional de Rosario in 1987 and a Masters in Economics from Universidad del CEMA in 1989, each in Argentina.

Author Jens Foehrenbach President and Co-CIO

Jens Foehrenbach, CFA, is the President and Co-Chief Investment Officer of Graham Capital Management, L.P. (“Graham”). Mr. Foehrenbach jointly oversees and supervises Graham’s discretionary and systematic portfolio manager teams, trading, and research, alongside Pablo Calderini, Vice Chairman and Co-Chief Investment Officer. Mr. Foehrenbach is also a member of the firm’s Executive, Investment, and Risk committees. Prior to joining Graham, he worked at Man Group from September 2008 to February 2025, most recently as Head of Public Markets within Discretionary Investments at Man Group. Mr. Foehrenbach has served in several capacities for the Man Group during his tenure at the firm, including Chief Investment Officer of Man Solutions and Chief Investment Officer of Man FRM. Prior to joining Man Group, Mr. Foehrenbach worked at Harcourt Investment Consulting AG as Senior Analyst and Head of Relative Value. Prior to Harcourt Investment Consulting AG, he was employed by UBS AG, where he worked on the bank’s fixed income derivatives trading desk in Switzerland and London. Jens Foehrenbach received a Master’s degree in Business Economics from the University of Basel, Switzerland in 2001.

DISCOSURE

This presentation includes statements that may constitute forward-looking statements. These statements may be identified by words such as “expects,” “looks forward to,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “will,” “project” or words of similar meaning. In addition, our representatives may from time to time make oral forward-looking statements. Such statements are based on the current expectations and certain assumptions of Graham Capital Management’s (“Graham”) management, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Graham’s control, affect the operations, performance, business strategy and results of the accounts that it manages and could cause the actual results, performance, or achievements of such accounts to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical trends.

This document is not a private offering memorandum and does not constitute an offer to sell, nor is it a solicitation of an offer to buy, any security. The views expressed herein are exclusively those of the authors and do not necessarily represent the views of Graham Capital Management. The information contained herein is not intended to provide accounting, legal, or tax advice and should not be relied on for investment decision making.

Tables, charts, and commentary contained in this document have been prepared on a best-efforts basis by Graham using sources it believes to be reliable although it does not guarantee the accuracy of the information on account of possible errors or omissions in the constituent data or calculations. No part of this document may be divulged to any other person, distributed, resold and/or reproduced without the prior written permission of Graham.

Subscribe to our Resource Center

By clicking the Button you confirming that you’re agree with our following Terms and Conditions

By clicking register you are confirming that you agree with our following Terms and Conditions

Welcome to Graham Capital Management

By entering this website you are agreeing to its Terms of Use.

The risk of loss in trading commodities can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

In some cases, managed commodity accounts are subject to substantial charges for management and advisory fees. It may be necessary for those accounts that are subject to these charges to make substantial trading profits to avoid depletion or exhaustion of their assets. The disclosure document contains a complete description of the principal risk factors and each fee to be charged to your account by the commodity trading advisor (“CTA”). The regulations of the commodity futures trading commission (“CFTC”) require that prospective clients of a CTA receive a disclosure document when they are solicited to enter into an agreement whereby the CTA will direct or guide the client’s commodity interest trading and that certain risk factors be highlighted. This brief statement cannot disclose all of the risks and other significant aspects of the commodity markets. Therefore, eligible investors should carefully study the disclosure document to determine whether such trading is appropriate for you in light of your financial condition. Eligible investors are encouraged to access the disclosure document by contacting Graham, which will be provided at no additional cost. The CFTC has not passed upon the merits of participating in this trading program nor on the adequacy or accuracy of the disclosure document. Other disclosure statements are required to be provided to you before a commodity account may be opened for you. By accepting the terms of this statement and entering the site you are confirming your understanding of this statement.

Any “benefit plan investor” (e.g. An IRA or other ERISA investor) investor is hereby deemed to represent to Graham Capital Management (“Graham”) that an independent fiduciary (as defined in the ERISA fiduciary rule) is exercising its independent judgment with regard to such investor’s investment in any Graham managed fund and is aware of and acknowledges and agrees that Graham and its affiliates are relying on the exception set forth in clause (c)(1) of the ERISA fiduciary rule (i.e., the “transactions with independent fiduciaries with financial expertise” exception) with respect to any communications made to the investor or the investor’s fiduciary that are considered recommendations concerning any transaction and such benefit plan investor.

Although the site may include investment-related information, nothing on the site is a recommendation that you purchase, sell or hold any security or other investment, or that you pursue any investment style or strategy.

We do not give any advice or make any representations through the site as to whether any investment is suitable to you or will be profitable.

Nothing on the site is intended to be, and you should not consider anything on the site to be, investment, accounting, tax or legal advice. If you would like investment, accounting, tax or legal advice, you should consult with your own financial advisors, accountants or attorneys regarding your individual circumstances and needs.

The past performance of any investment, investment strategy or investment style is not indicative of future performance.

If you have been provided with a password to access the site you are solely responsible for maintaining the confidentiality and security of your password. You may not disclose your password to any third party. You accept full responsibility for any use of your password. You must notify Graham immediately of any actual or suspected loss, theft or unauthorized use of your password.

We are not obligated to inquire as to the authority or propriety of any use of or action taken under your password. We will not be responsible for any loss to you that arises from such use or action or from your failure to comply with these provisions.

The site, including all content, is provided as is and as available.

We disclaim all representations and warranties, express or implied, of any kind with respect to the site and the content including warranties of merchantability, fitness for a particular purpose and non-infringement of intellectual property and proprietary rights.

Without limiting our general disclaimer, we do not warrant the availability, accuracy, completeness, timeliness, functionality, reliability, sequencing or speed of delivery of the site or the content.