For more than a decade following the Global Financial Crisis, markets operated in an environment defined by low inflation, suppressed volatility, and extraordinary policy support. This paper argues that those conditions were not permanent, but rather the product of a unique macroeconomic and policy regime that has since broken down. As supply constraints, persistent inflation, deglobalization, and more active fiscal policy reshape the economic landscape, volatility is increasingly becoming a structural feature of markets rather than a temporary disruption. The result is a growing disconnect between how markets are priced and how the system now functions.

Key Takeaways

- The post-GFC low-volatility regime was artificially supported by low inflation and aggressive central-bank policy but those conditions no longer exist.

- Markets are still priced for the old environment, leaving assets and traditional portfolios more vulnerable to structural volatility and repricing.

- Inflation and supply constraints have made policy support more limited and less predictable.

- Traditional diversification strategies may be less effective in a higher-volatility regime.

INTRODUCTION

A common view is that the pandemic volatility shock was just that: a shock. An exogenous disruption that temporarily pushed markets and the economy off course, but one that is now largely behind us. Inflation has moderated, markets have stabilized, and it is tempting to believe the system is gradually returning to something like the pre-pandemic environment.

Our view is different. We do not believe the pandemic was a one-off disruption to a stable low-volatility regime but was instead the catalyst that exposed the limits of that regime and forced an exit from it. We will argue in this piece that the stability of the post-GFC period was never a natural equilibrium. It depended on a specific macroeconomic backdrop: weak demand, low inflation, disinflationary globalization, and a policy framework able to suppress volatility and inflate asset prices. Those conditions no longer reliably hold.

The result is not simply a more volatile version of the old environment. It is a different regime: one defined by more binding supply constraints, less stable inflation, more active fiscal policy, and a policy framework that is more constrained and less predictable. In that world, volatility is not as easily suppressed. It becomes a structural feature of the system.

Markets have not fully internalized that shift. Asset prices, risk premia, and portfolio construction still reflect assumptions forged in the post-GFC regime, even as the foundation for those assumptions has eroded. The mismatch between how the system is priced and how it now functions is the central risk this piece explores.

HOW AND WHY THE LOW-VOLATILITY REGIME WAS ENGINEERED

To understand why that regime was transitory, it is necessary to understand what created it. The low-volatility environment that followed the Global Financial Crisis was not simply a byproduct of subdued inflation or calmer markets. It emerged from a specific macroeconomic problem, debt deflation, and a specific policy response, asset price reflation.

Debt deflation is dangerous because falling asset prices weaken balance sheets, force deleveraging, reduce credit creation, and push asset prices lower still, creating a self-reinforcing downward spiral. The policy response was therefore clear. If falling asset prices were the problem, rising asset prices were the solution. After the GFC, the Federal Reserve and other major central banks pursued that goal through zero- and negative-rate policy, quantitative easing, forward guidance, and direct asset purchases. These tools did not just stimulate demand. They changed the market pricing of risk: duration risk, term premia, credit risk, equity risk, and volatility itself. Policymakers were not simply trying to restart growth. They were trying to reflate the asset base of the economy.

The Mechanics of Volatility Suppression

Put another way, the tools used to stabilize the post-GFC economy worked in part by suppressing specific market risks. Policymakers could not quickly improve the fundamentals underlying asset prices, but with trillion-dollar balance sheets, they could engineer higher prices by distorting the risks embedded in those prices. Quantitative easing reduced duration risk by removing long-term bonds from the market, inflating the price of duration and, by extension, all long-duration assets from bonds to low-current-cash-flow equities and beyond. Forward guidance compressed uncertainty around the future path of short rates, lowering term premia, and making near-term cash flows less attractive relative to more uncertain, longer-duration ones. Zero-rate policy reduced the time value of money and pushed investors outward along the risk curve. Together, by broadly compressing risk premia, these policies lowered credit spreads, inflated valuations for the longest-duration equities, reinforced the correlation structure that underpinned risk parity and 60/40 portfolios, supported private equity, and made volatility itself appear less risky. But because that market structure depended on inflation remaining low enough for policymakers to keep suppressing risk, it was always more conditional than it appeared.

The Pandemic and the Regime Shift

The pandemic initially triggered an even more aggressive version of the post-GFC policy response. Rates returned to zero, the Fed’s balance sheet nearly doubled from roughly $4 trillion to almost $9 trillion, and fiscal policy was deployed on a scale far beyond the prior cycle, with pandemic relief legislation totaling roughly $5 trillion versus less than $1 trillion for the American Recovery and Reinvestment Act after the GFC.

But unlike the post-GFC period, the result was not a prolonged demand shortfall and subdued inflation. It was a rapid recovery in nominal demand, disrupted supply, and the first sustained inflation shock in decades. Once inflation became binding, the Fed was forced to reverse the very policies that had supported the low-volatility regime. Rates rose sharply, balance sheet policy shifted from expansion to runoff, term premia began to reprice, and the negative stock-bond correlation that underpinned the 60/40 portfolio broke down. In 2022, a traditional 60/40 portfolio declined roughly 16–18%, depending on construction, one of its worst performances in modern history. Morgan Stanley estimated 2022 was the worst year for a 60/40 portfolio since 1937 and the fourth-worst in roughly 200 years1.

The issue was not simply that the pandemic was an extreme shock. It was that an extreme shock hit a market structure engineered to treat extreme shocks as unlikely, temporary, and ultimately containable. In that sense, the pandemic did not merely interrupt the low-volatility regime; it exposed the condition on which it had always depended: inflation had to remain low enough for policymakers to keep suppressing market risk.

As markets stabilized, it became tempting to view the pandemic and inflation shock as a one-off disruption to an otherwise durable low-volatility regime. But the low-volatility regime was not a stable equilibrium to which the economy would necessarily naturally return. In this piece, we will argue that low-volatility regime was a conditional construct that depended on macroeconomic and policy conditions that no longer reliably exist. Put simply, when low and stable inflation can no longer be taken for granted, the asset-inflating policies that defined the post-GFC regime can no longer be relied upon either.

The sections that follow explain why the conditions that made volatility suppression possible have eroded.

WHY THE CONDITIONS THAT SUPPRESSED VOLATILITY HAVE BROKEN DOWN

The low-volatility regime was not a naturally occurring phenomenon but was instead the product of a policy framework designed to suppress market risk and inflate asset prices. While policymakers still want to support markets, the question is whether they can still do so without creating larger problems elsewhere. In a higher-inflation environment, easing policy to support markets can backfire by reigniting inflation pressure, pressuring bond yields, and creating new instability. Thus, even as the desire for a policy put may still exist, exercising that put now risks creating the very instability it is meant to prevent.

1. The Economy is More Supply-Constrained Than Demand-Constrained

The post-GFC period was defined by insufficient demand. Volatility was largely tied to growth scares, financial stress, and recurring concerns that the recovery would stall. Those were risks policymakers could offset with easier policy. Lower rates, QE, and forward guidance worked because the economy had spare capacity and inflation was persistently subdued. Liquidity support lifted asset prices and supported demand without immediately creating an inflation problem.

Today, the constraint looks different. The economy appears less demand-deficient and more supply-constrained. Labor force growth has slowed as the population ages, immigration policy has become more volatile, and lower breakeven job growth means the labor market can tighten even with employment gains that would once have looked modest. At the same time, energy, housing, infrastructure, and supply chains have more visible bottlenecks. Even AI, the clearest potential source of faster supply-side growth, is already running into physical constraints. The data-center buildout is colliding with shortages of electricity, grid capacity, transformers, switchgear, batteries, skilled labor, and construction capacity. Bloomberg recently reported that almost half of U.S. data centers planned for this year are expected to be delayed or canceled because of shortages in electrical equipment, and this was before any further supply disruptions that may come from the Iran conflict2.

That changes the policy tradeoff. In a demand-constrained economy, liquidity is stabilizing: it lifts asset prices, supports demand, and does not immediately threaten inflation. In a supply-constrained economy, the same liquidity is more dangerous. It pushes demand into bottlenecks, raises prices, and forces policymakers to choose between supporting markets and preserving inflation credibility.

2. Inflation Can No Longer Be Treated as Dormant

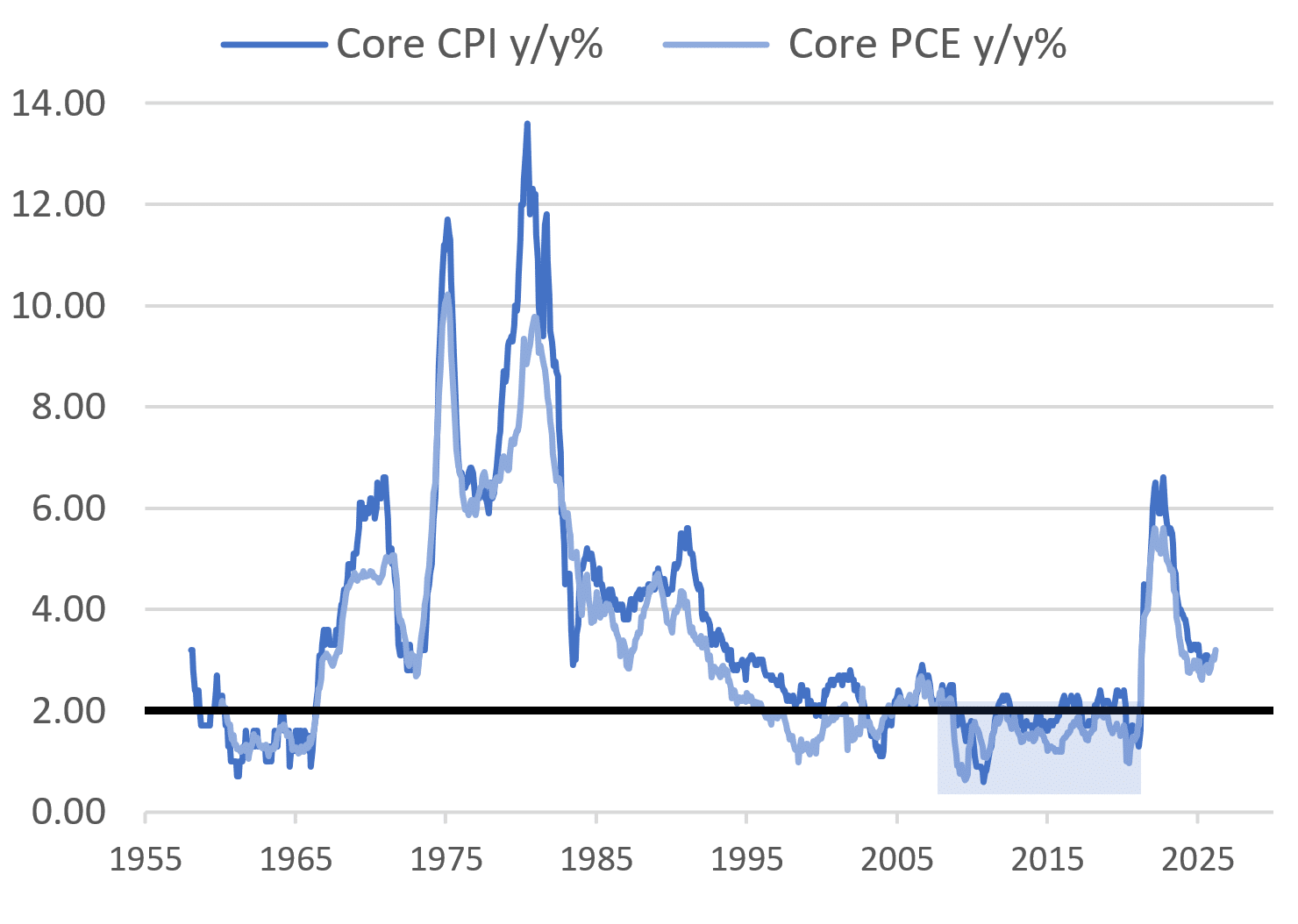

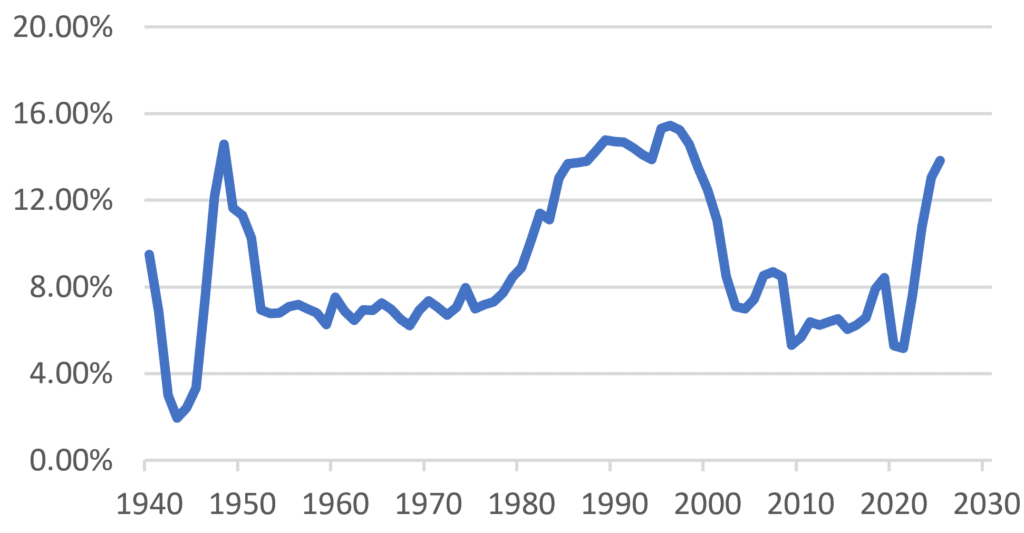

Inflation can no longer be assumed to be safely contained. In the post-GFC period, inflation was persistently too low: core PCE inflation averaged below the Fed’s 2% target for most of the decade following the crisis, even as unemployment fell below 4% by 2018. Structural forces like demographics, globalization, technology, and anchored expectations were keeping inflation subdued and the persistence of those factors gave the Fed and other major central banks room to keep policy easy, use forward guidance and balance-sheet expansion. Those policies suppressed volatility and supported asset prices with few immediate inflationary consequences.

The pandemic broke that assumption. It showed that when policy supports demand into a constrained supply environment, inflation can re-emerge quickly and forcefully. More importantly, it showed that inflation is not as inert as previously believed. It is not simply a lagging outcome that can be managed over time, but a variable that can move rapidly when conditions change.

Inflation is No Longer Consistently Low and Stable

The pandemic may also have changed pricing behavior itself. After a long period in which firms were reluctant to raise prices and consumers were conditioned to expect price stability, the inflation shock made price increases more visible, more frequent, and more accepted as a response to cost pressure. That does not mean inflation will remain high indefinitely, but it does suggest pricing behavior may be more dynamic than it was during the post-GFC period. In that environment, inflation can become less inert and more responsive to shocks.

Core PCE Inflation (%y/y)

This fundamentally changes the policy framework. There is an obvious incentive, from both policymakers and markets, to return to the pre-pandemic model. But as the economy has suffered from persistent supply constraints, inflation has also proven more persistent than hoped. At the same time, asset markets remain acutely sensitive to sharp moves higher in government bond yields, and policymakers can no longer assume that weakness in growth or markets will automatically create room to ease. The Fed is now operating with a constraint that was largely absent in the post-GFC period: the risk that policy support itself reignites inflation.

3. Globalization Is No Longer a Reliable Disinflationary Force

The pandemic also exposed the limits of globalization as a volatility suppressor. In the post-GFC period, global supply chains helped keep goods prices low and allowed shocks to be absorbed across a broad, flexible production network. That was part of what made inflation look structurally contained. Even when demand improved, firms could rely on global labor, cheaper imported goods, and just-in-time production to limit cost pressures.

That dynamic started to break during the pandemic. Supply chains that had been optimized for efficiency proved more fragile than expected, and the initial shortages made clear that low-cost production was not the same thing as resilient production. Since then, the shift has accelerated. Tariffs, industrial policy, export controls, reshoring, and the deterioration of diplomatic alliances have all pushed the system further away from maximum efficiency and toward redundancy, security, and political control.

That shift may be justified from a national security or resilience perspective, but it is not disinflationary. A world with more fragmented supply chains, more trade barriers, and more politically directed production is a world with less elastic supply and higher costs. Shocks that might once have been absorbed through global production networks are now more likely to persist, feed into prices, and complicate policy.

This is not just a U.S. story. The broader environment that helped suppress inflation has also shifted. Europe has moved away from austerity toward more active fiscal policy, reducing a key source of demand restraint. Japan, long a source of persistent disinflation, is now experiencing sustained inflation and shifting away from ultra-loose policy. The post-Brexit U.K. has become an example of how reduced trade openness and a less elastic labor supply can leave an economy more vulnerable to persistent inflation. More broadly, geopolitical fragmentation, trade barriers, and shifting alliances are making the system less efficient and less disinflationary.

4. Fiscal Policy Has Become a Source of Volatility

Another important shift is the role of fiscal policy. In the post-GFC period, fiscal policy was generally more constrained, particularly in the U.S. After the initial crisis response, many advanced economies moved toward austerity or at least fiscal restraint, in part because markets had become more intolerant of high and rising sovereign debt burdens. Europe was the clearest example: countries with the weakest fiscal positions experienced the sharpest sovereign bond-market volatility, with spreads and yields in countries like Italy and Greece rising sharply, while countries with stronger balance sheets were less exposed. That distinction matters because it shows that fiscal sustainability itself can become a source of market instability. In the post-GFC period, that pressure pushed policy toward restraint, reinforcing the demand shortfall and reducing pressure on inflation.

Fiscal restraint also supported the low-volatility goals of monetary policy more directly. Lower deficits meant reduced Treasury issuance, which helped keep term premia and duration risk contained. Combined with QE, this created a powerful dynamic: central banks were removing duration from the market at the same time that governments were not meaningfully increasing its supply. The result was a structurally lower level of long-term yields, compressed risk premia, and reduced rate volatility. Fiscal and monetary policy were aligned in actively suppressing market risk.

Annual Fiscal Deficits Remain Historically Large Outside Recession

That alignment has broken down. Fiscal policy has become larger, more persistent, and less tied to the cyclical stabilization role it played in the post-GFC framework. The pandemic marked a clear turning point, with deficits expanding dramatically and fiscal support continuing well into the recovery. Since then, fiscal policy has remained active through industrial policy, defense spending, energy transition investments, and supply-chain resilience programs, including legislation such as the CHIPS Act, the Inflation Reduction Act, and increased defense commitments.

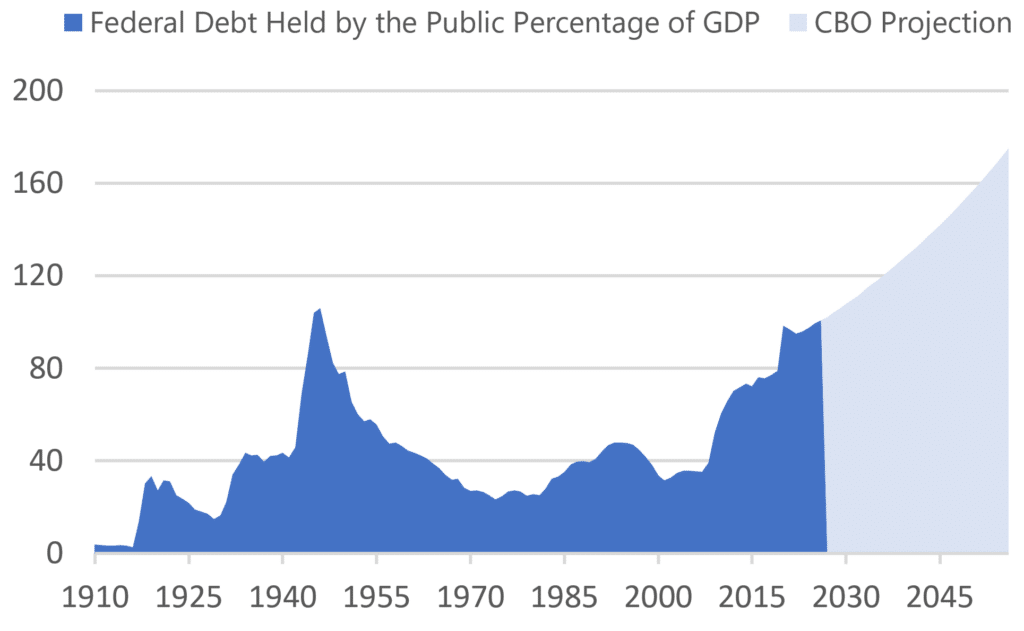

Federal Debt to GDP Exceeded 100% This Year, The First Time Since WWII

The issue is not just the scale of fiscal policy, but also its composition. More recent fiscal support has often been directed toward defense, transfers, subsidies, industrial policy, and energy security rather than higher-multiplier public investment. To the extent that this spending sustains demand without generating a commensurate increase in near-term supply, it can be more inflationary and less growth-enhancing. That makes fiscal policy a less reliable stabilizer and a more direct source of volatility.

Fiscal policy now works in the opposite direction of the post-GFC regime. Instead of reinforcing demand weakness, it can amplify demand at a time when supply is already constrained. Larger deficits also mean increased Treasury issuance, which can put upward pressure on long-end yields even as the Fed attempts to manage financial conditions. In that environment, efforts to support markets, whether through easier monetary policy, fiscal stimulus, or public pressure to keep financial conditions loose, can be offset or even overwhelmed by the bond market’s reaction to fiscal expansion.

Interest Costs are Climbing Towards Levels Last Seen During the Inflation Crisis

5. Economic Signals Are Harder to Interpret

While all these changes have occurred, the economy itself has become harder to read. In the post-GFC period, growth was weak, but the underlying structure of the economy was relatively stable. Estimates of labor supply, potential growth, and slack were imperfect, but they were not moving targets. Policymakers could make decisions with a reasonable degree of confidence about the economy they were trying to manage.

That is less true today. Key inputs into monetary policy are more uncertain and more dynamic. Productivity may be shifting because of AI, but the timing and magnitude are unclear. Labor supply is being reshaped by aging and reduced immigration, making it harder to know how tight the labor market really is. Recent Fed staff research3 has argued that slower labor-force growth may have reduced breakeven employment growth to near zero, meaning payroll gains that once would have signaled expansion may now be consistent with a tightening labor market. At the same time, declining resources at government statistical agencies4 have introduced additional measurement error, making the data themselves less reliable just as the economy has become harder to interpret. The relationship between growth, wages, and inflation has also become less stable.

That instability makes the key inputs into policy harder to estimate in real time: actual growth, potential growth, and the neutral policy rate. Policymakers are forced to infer the state of the economy from less reliable data that can support multiple, often conflicting interpretations. Strong growth could reflect improved supply or overheating demand. Slower hiring could signal weakness or simply a lower labor force growth rate. Sticky inflation could reflect demand, supply constraints, or both.

This uncertainty matters because policy is set based on those inferences. In a recent speech, Fed Governor Christopher Waller raised the possibility that the Fed may have misread weak payroll gains as labor-market deterioration when they may have instead reflected sharp declines in labor availability5. If policymakers had understood that distinction in real time, it is not clear they would have eased as they did. That is exactly the kind of observability problem that can turn into policy error. Because those mistakes are only revealed with a lag, the eventual adjustment may need to be larger and more abrupt. In that sense, the challenge is no longer just uncertainty but also unobservability, and that makes for a less stable backdrop for both policy and markets.

Taken together, these changes mean the policy framework that suppressed volatility after the GFC has fewer degrees of freedom. Weak demand, low inflation, elastic global supply, fiscal restraint, and stable financial conditions gave policymakers room to ease aggressively without immediately creating offsetting risks. That room has narrowed. Policy support can still stabilize markets, but it can also push demand into bottlenecks, reignite inflation pressure, raise long-end yields, weaken credibility, or force a larger adjustment later. The policy put has not disappeared, but it has become more costly to exercise and therefore less reliable.

MARKETS ARE STILL PRICED FOR THE OLD REGIME

If the post-GFC regime was defined by suppressed volatility, compressed risk premia, and a policy framework that reliably supported asset prices, then the implications of its reversal are not subtle. Markets are still priced as if much of that regime remains intact, even as the conditions that supported it have weakened.

The starting point is the price of risk. Risk premia are often discussed as abstract valuation concepts, but in practice they determine how much leverage the system can support, how expensive hedging is, how tight credit spreads can remain, how high equity multiples can go, and how low long-end yields can stay. When risk premia are compressed, the same cash flows support higher asset prices. When risk premia rise, those prices fall, even if the cash flows themselves have not changed.

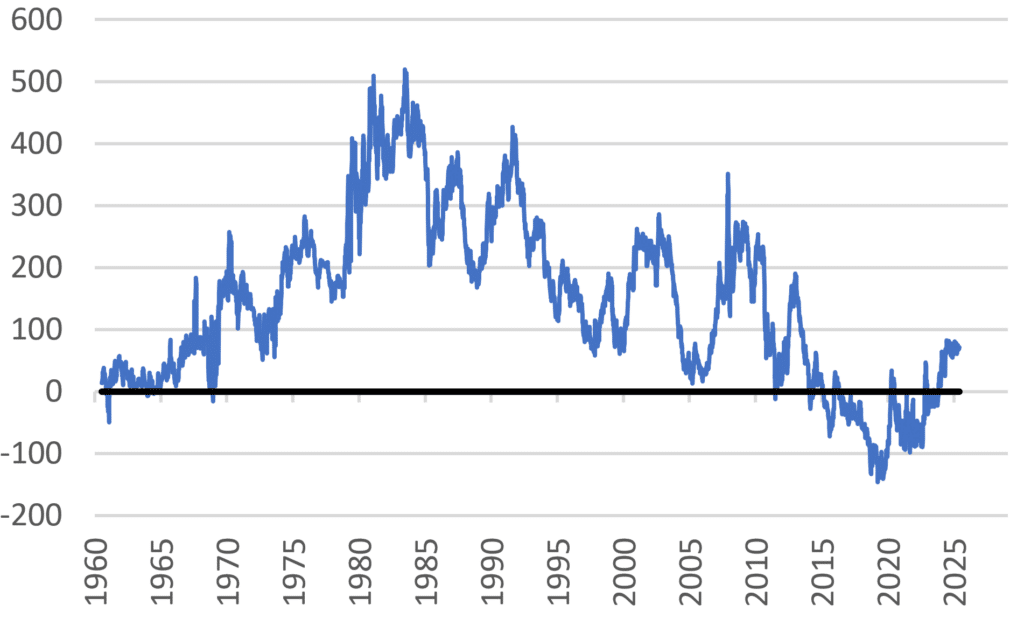

Term premia are the clearest example. By 2019, term premia had fallen to roughly -150 basis points, a level difficult to justify under any normal understanding of risk pricing. Investors were not merely receiving too little compensation for duration risk. They were effectively paying to hold it. As inflation returned and the Fed tightened policy, term premia moved toward roughly +50 basis points. That repricing was part of the broader rate shock that helped break the traditional 60/40 portfolio in 2022.

Markets may be treating that repricing as finished when it was only the first adjustment. Even after the move from deeply negative levels, term premia remain well below longer-run averages and far below levels reached when inflation risk was priced more aggressively. What markets are treating as a completed adjustment may still reflect a significant degree of complacency. If the macro environment has changed, a further move higher in term premia would raise long-end yields even without a change in expected short rates, tighten financial conditions, pressure equity multiples, and force investors to reprice long-duration assets across the system.

ACM 10yr Treasury Term Premium

That is why term premia matter. They are not an abstract bond-market concept. They are one of the prices that determine the valuation of every long-duration asset in the system. When term premia are low, long-duration assets look safer, equity multiples can rise, bonds can hedge equities, credit spreads can remain tight, and leverage can build. When term premia rise, all of that changes.

This is the broader mistake markets may be making. Many of the features investors came to treat as constants were actually regime-specific variables. Negative stock-bond correlation was not a permanent law of portfolio construction; it depended on low and stable inflation. Higher valuations for long-duration equities were not a permanent feature of superior business models; they depended on low discount rates and low required returns. Tight credit spreads were not simply evidence of stronger corporate fundamentals; they were partly the result of investors being pushed outward along the risk curve. Private equity valuations were not insulated from the public-market regime; they were one of its clearest expressions.

That is the key point. The post-GFC regime did not just raise asset prices. It changed the way investors understood risk. It made duration look safer, leverage look more sustainable, illiquidity look less costly, and volatility look more suppressible. Those assumptions worked because inflation was low, policy was predictable, and central banks could respond to weakness by easing. If those conditions no longer hold, then the assumptions built on top of them no longer hold either.

THIS IS HOW THE OLD ASSUMPTIONS BREAK

If the assumptions of the post-GFC regime are still embedded in prices, then the consequences are not theoretical. Many assets and portfolios still reflect assumptions about inflation, policy, and risk that no longer reliably hold. As those assumptions are tested, the adjustment will show up in how risk is priced across markets. Some of that adjustment has already happened. The mistake is assuming it is finished.

1. High Multiples Do Not Need Weak Earnings to Fall

High equity multiples are one place where the mismatch is most visible. U.S. equities remain historically expensive, with the S&P 500 trading around 22x forward earnings, above its 30-year average of roughly 17x6, while the CAPE ratio is near 38x, more than double its long-run average of roughly 17x7. The issue is not simply that valuations are high. It is that they are high for reasons that may no longer be valid.

The multiple expansion of the post-GFC period was not driven by earnings alone. It was driven by falling discount rates, compressed term premia, suppressed volatility, and the expectation that policymakers would cushion drawdowns. Those conditions made future cash flows look more valuable and reduced the compensation investors demanded for uncertainty.

A rerating would still likely require a catalyst, so this is not a near-term market call. But the vulnerability is already embedded in the starting valuation. If the forward multiple merely returned to its long-run average, that would imply roughly 20% downside before any change in earnings. If multiples moved to levels more consistent with higher inflation or higher-volatility environments, the adjustment would be larger. The point is not the precise downside estimate. The point is that equities do not need an earnings collapse to fall. The same stream of cash flows can support a lower price simply because investors demand more compensation to hold it.

A valuation reset does not require a recession or a replay of the 1970s. It only requires investors to stop paying post-GFC multiples for cash flows in a world that no longer supports post-GFC assumptions.

2. Smooth Marks Are Not the Same as Low Risk

The same dynamic is visible in private credit and other illiquid assets. Their appeal has been the ability to generate stable income with limited mark-to-market volatility. But that stability is, in part, a function of how the assets are priced.

Less frequent pricing can make volatility look lower without making the underlying risk lower. In an environment of low rates, abundant liquidity, and easy refinancing conditions, that distinction mattered less. Defaults were low, capital was readily available, and time worked in the investor’s favor.

That environment is less reliable now. Higher rates, tighter financial conditions, and greater macro volatility make refinancing more uncertain and increase the importance of liquidity. In that world, the absence of daily marks does not eliminate volatility. It delays its recognition.

The risk is that illiquidity has been treated as a source of return rather than a source of risk. In a regime where the price of risk rises, illiquidity should require more compensation, not less.

3. Diversification Still Depends on the Inflation Regime

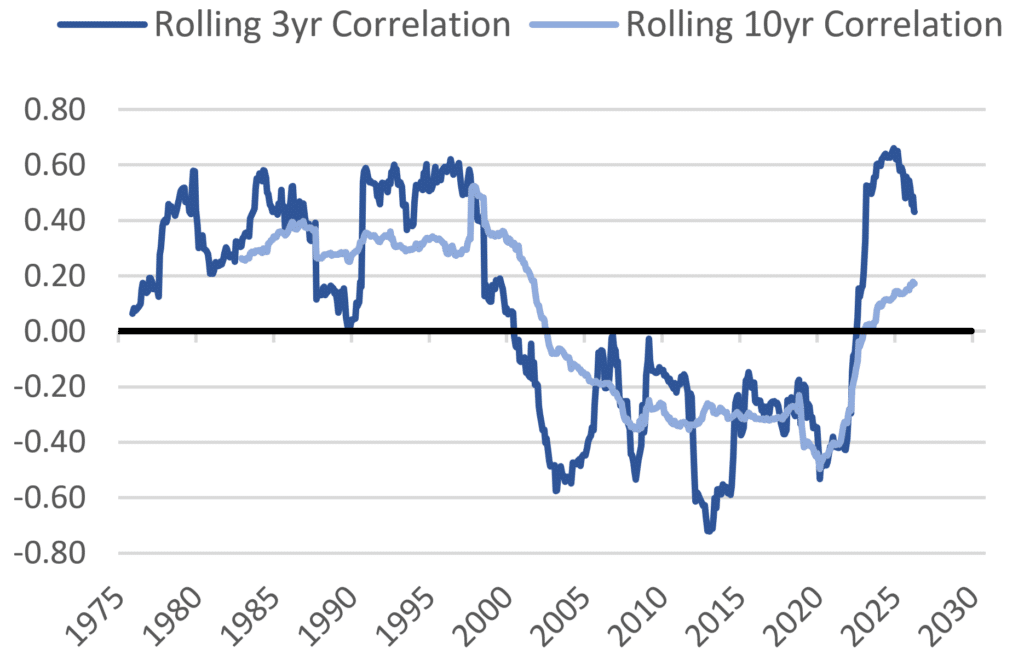

One of the most important assumptions carried forward from the post-GFC period was that bonds would reliably diversify equity risk. That assumption mattered most for risk parity and other volatility-targeted strategies, which depended not only on bonds rallying when equities fell, but on the stock-bond correlation remaining stable enough to support leverage. The traditional 60/40 portfolio benefited from the same structure, but risk parity, which gained traction in the post-GFC period, was more directly exposed to it. When inflation shocks pushed stocks and bonds down together in 2022, the problem was not simply that bonds failed to hedge equities. It was that a core input into the portfolio construction process had changed.

Rolling Monthly Stock Bond Correlation

That relationship is not a law of nature. It depends on the inflation regime. In a low and stable inflation environment, shocks tend to be growth shocks. Policy can ease in response, bond yields fall, and bonds hedge equities. That dynamic underpinned the performance of balanced portfolios for much of the post-GFC period.

In a higher and less stable inflation environment, that relationship becomes less reliable. Shocks are more likely to be inflation shocks, or a combination of inflation and growth. In that case, policy cannot respond as easily, bond yields can rise alongside equity volatility, and the hedge weakens or disappears.

That is what happened in 2022, when both stocks and bonds declined sharply. The point is not that diversification no longer works. It is that diversification is conditional. Portfolios that appear diversified across asset classes may still be concentrated in a single underlying assumption: that inflation remains low and that policy can respond to weakness without constraint.

4. Regime Change Looks Like a Series of One-Off Shocks

If the repricing of risk is not complete, it is unlikely to happen in a smooth or linear way. Regime changes rarely do. They tend to unfold through events that initially appear unrelated.

That is what this period has felt like. Even after the pandemic volatility seemed to have passed and markets tried to return to the old normal, the shocks continued. August 2024 brought a sharp global selloff tied to recession fears, crowded positioning, and the yen carry-trade unwind. April 2025 brought tariff-driven volatility and a sharp move higher in Treasury yields. March 2026 brought another broad selloff, this time tied to tariffs, AI-capex concerns, private-credit liquidity worries, and geopolitical risk. Each episode had its own catalyst. But the frequency matters. When large disruptions keep arriving every few months, the better question is whether they are really isolated shocks at all.

Each episode can still be explained in isolation. That is what makes the transition difficult to recognize in real time. The impulse is to interpret each shock through the old framework: volatility will fade, policy will respond, markets will stabilize. That was often the right reflex in the post-GFC regime.

In a different regime, that reflex can be misleading. What looks like a series of temporary disruptions may instead be the process through which risk is repriced. The adjustment does not need a single defining event. It can emerge through repeated shocks that stop looking isolated only in hindsight. Regime changes are not recognized as regimes until repeated “one-off” shocks stop looking isolated.

The economy is increasingly leveraged to asset prices not falling, while the tools used to support those prices are increasingly constrained by inflation, deficits, and the bond market. That is the tension running through this regime shift. The policy put has not disappeared, but it is less reliable, less powerful, and more costly to exercise. The excesses of the post-GFC regime have not been fully unwound. They have been carried forward into a new environment that is less capable of sustaining them. Markets are still priced for stability in a system that is becoming structurally less stable.

CONCLUSION

After a rupture, continuity is the most seductive illusion: the belief that the old order is still there, temporarily obscured but fundamentally intact. For more than a decade, that instinct was not only understandable; it was profitable. It was also enforced by central banks, which penalized investors who positioned against it. The post-GFC regime trained investors to think in a certain way: buy duration, buy dips, own the market, accept illiquidity, add leverage, trust that bonds would hedge equities, and assume that policymakers would eventually step in. Those were not irrational choices. They were the correct choices for a world of low inflation, weak demand, compressed risk premia, and policy-suppressed volatility. But they were regime-specific choices, not universal truths — and habits formed in one regime can become liabilities in the next.

If the regime has changed, then the question is not whether 60/40 is “dead,” whether equities are “too expensive,” or whether bonds “work” again. Those questions are too narrow. The better question is whether investors are still using a playbook built for a world that no longer exists. A 60/40 portfolio may still look diversified, but if both sides depend on low inflation and low term premia, it is less diversified than it appears. Private assets may still look smooth, but smoothing is not the same thing as safety. Long-duration equities may still have great businesses behind them, but great businesses can still be bad assets at the wrong discount rate.

The trade, broadly speaking, is not to assume disaster. It is to stop assuming rescue. It is to stop treating volatility as a policy mistake that will always be corrected and start treating it as a feature of the new environment. That means caring more about valuation, cash flow timing, liquidity, inflation sensitivity, and whether the hedge is really a hedge. It means recognizing that many portfolios that look diversified by asset class may actually be concentrated in one underlying exposure: the assumption that risk will remain underpriced.

Regime changes are rarely recognized cleanly in real time. They often arrive as a series of events that look separate at first: an inflation shock, a bond bear market, a 60/40 drawdown, a yield spike, a growth scare. Each can be explained away on its own. But taken together, they may be evidence of something larger: not repeated disruptions to the old regime, but the emergence of a new one.

The low-volatility regime made leverage look prudent, illiquidity look safe, long-duration cash flows look inherently superior, and diversification look almost automatic. A higher-volatility regime is likely to reverse that illusion. It does not eliminate opportunity, but it changes where opportunity lies. It favors assets whose returns come from current cash flows and reasonable starting valuations, not from falling discount rates, multiple expansion, or policy rescue. The opportunities will still be there, but not for portfolios built on yesterday’s assumptions. Those assumptions will be obstacles, not guides.

IMPORTANT DISCLOSURE

REFERENCES

1 Morgan Stanley Investment Management. ‘BIG PICTURE: Return of the 60/40.’ Morgan Stanley Investment Management, April 2024, https://www.morganstanley.com/im/publication/insights/articles/article_bigpicturereturnofthe6040_ltr.pdf. Accessed 5/13/2026.

2 Bloomberg. ‘US Data Center Boom Relies on Hard-to-Find Electrical Equipment.’ Bloomberg, April 1, 2026, https://www.bloomberg.com/news/newsletters/2026-04-01/us-data-center-boom-relies-on-hard-to-find-electrical-equipment. Accessed 5/13/2026.

3 Board of Governors of the Federal Reserve System. ‘Labor Force Growth, Breakeven Employment, and Potential GDP Growth.’ Federal Reserve, April 2, 2026, https://www.federalreserve.gov/econres/notes/feds-notes/labor-force-growth-breakeven-employment-and-potential-gdp-growth-20260402.html. Accessed 5/13/2026.

4 U.S. Bureau of Labor Statistics. ‘Notice of CPI Collection Reductions.’ Bureau of Labor Statistics, 2025, https://www.bls.gov/cpi/notices/2025/collection-reduction.htm. Accessed 5/13/2026.

5 Board of Governors of the Federal Reserve System. ‘Labor Market Data: Signal or Noise?’ Federal Reserve, February 23, 2026, https://www.federalreserve.gov/newsevents/speech/waller20260223a.htm. Accessed 5/13/2026.

6 J.P. Morgan Asset Management. ‘Guide to the Markets.’ J.P. Morgan Asset Management, https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/. Accessed 5/13/2026.

7 Shiller, Robert. ‘Online Data Robert Shiller.’ Yale University Department of Economics, http://www.econ.yale.edu/~shiller/data.htm. Accessed 5/13/2026.

LEGAL DISCLAIMER

This presentation includes statements that may constitute forward-looking statements. These statements may be identified by words such as “expects,” “looks forward to,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “will,” “project” or words of similar meaning. In addition, our representatives may from time to time make oral forward-looking statements. Such statements are based on the current expectations and certain assumptions of Graham’s management, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Graham’s control, affect the operations, performance, business strategy and results of the accounts that it manages and could cause the actual results, performance or achievements of such accounts to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical trends.

This document is not a private offering memorandum and does not constitute an offer to sell, nor is it a solicitation of an offer to buy, any security. The views expressed herein are exclusively those of the authors and do not necessarily represent the views of Graham Capital Management. The information contained herein is not intended to provide accounting, legal, or tax advice and should not be relied on for investment decision making.