Our Q2 2026 outlook reflects a shift from cyclical reacceleration to a more fragile macro regime shaped by geopolitical disruption and structural uncertainty. The Iran-driven energy shock has altered the landscape, introducing risk premia across energy, trade, and policy even amid a tentative ceasefire that appeared close to collapsing less than a week after its announcement. Markets now face constrained supply channels and elevated volatility on top of institutional uncertainty around central bank policy and the Fed leadership transition. As a result, the outlook is defined by slower, less stable growth, higher term premia, and a wider range of potential outcomes.

Key Takeaways

Geopolitics reshapes the macro regime: The Iran-driven energy shock has shifted markets from a cyclical growth story to one defined by supply constraints, chokepoints, and persistent risk premia.

Growth outlook turns more fragile: While recession is not imminent, risks have tilted toward more fragile U.S. growth and more persistent inflation as energy costs, tighter credit, and policy uncertainty weigh on activity.

Execution over conviction: Elevated volatility, weaker diversification, and rising term premia make sequencing, risk management, and adaptability more critical than forecasts.

A World of Chokepoints

Looking back to last year, in our July 2025 outlook, we argued that the U.S. economy would reaccelerate into late 2025 and early 2026. Up until the end of February, that view broadly looked right. The Federal Reserve’s March projections showed median 2026 real GDP growth of 2.4%, unemployment at 4.4%, and both headline and core PCE inflation at 2.7%. We had expected even stronger growth, driven by capex, onshoring, and tax incentives. Recent labor data remained soft but did not, on their face, depict an economy heading into recession. The economy started the new year in a fragile equilibrium that could tolerate noise; what it got instead was a genuine geopolitical supply shock.

That is what changed on February 27. The Iran war did not simply add another risk factor; it changed the character of the macro regime. The Strait of Hormuz is not a marginal channel: in 2024 and early 2025, it accounted for more than one-quarter of global seaborne oil trade, about one-fifth of global oil and petroleum product consumption, and around one-fifth of global LNG trade. Iran used its geography as asymmetric leverage, resulting in what the IEA described as the largest supply disruption in the history of the oil market.

The temporary ceasefire reduces the immediate tail risk, but – even if it holds, which at the time of writing appears questionable – it may not restore the old equilibrium. Iran is demanding tolling rights as part of its proposal, a reminder that a ceasefire is not the same thing as restored freedom of navigation. That distinction matters for markets. A world in which missiles stop flying but shipping remains politically conditioned is still a world with a structural energy premium, persistent freight friction, and an embedded geopolitical tax on growth. Tail risk is at this moment lower than it was in mid-March, and what is clear is that we are entering a new macro regime.

This is why the right framework for Q2 is not “war or no war.” It is a world of choke points. The trade confrontation with China already showed how concentrated supply chains can be weaponized, whether through rare earths, batteries, or other strategic inputs. The Iran conflict adds the energy analogue. The result is a macro regime in which availability matters as much as price, and in which volatility around the policy path is itself priced into markets; hence, markets charge an uncertainty premium. That framing is consistent with our January outlook, which argued that 2026 would be a transition year marked by higher term premia, less reliable cross-asset hedges, and a wider distribution of outcomes as policy volatility becomes institutionalized in prices.

A Violent Reaction Function

That brings us to March. It was one of the largest developed-market rates volatility shocks in years, driven by violent swings in front-end rates as markets flipped from pricing easing to pricing tightening. What made the episode particularly unusual was that this repricing occurred in response to heightened geopolitical uncertainty, conditions under which rates typically rally on safe-haven demand rather than sell off. Instead, markets initially interpreted the shock through an inflation lens, pushing yields higher even as risk assets came under pressure.

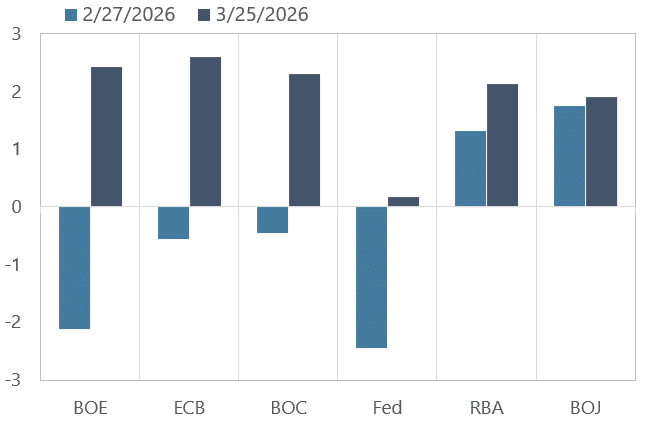

Number of Cuts/Hikes Priced by Year-End

Data Source: Bloomberg; Chart by Graham Capital Management

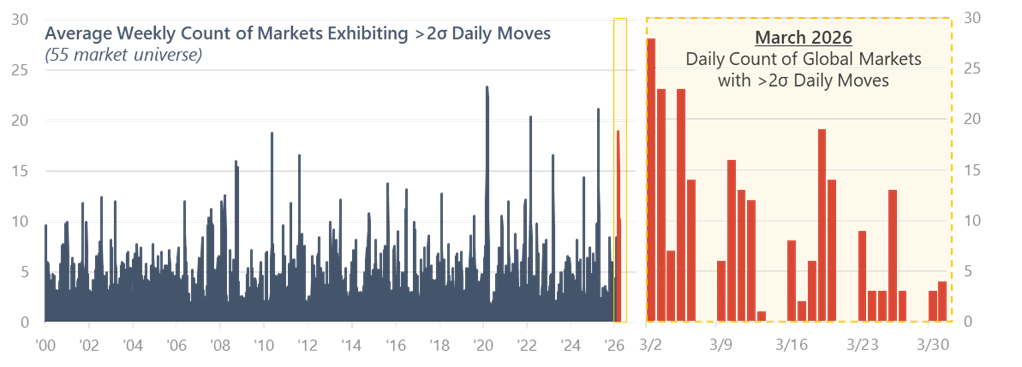

But the market reaction wasn’t limited to interest rates. A large share of liquid macro markets experienced tail events in early March.

“Big Days” – Number of Markets Exhibiting Tail Events

Source: Graham Capital Management; Computed over a 6-month daily lookback window

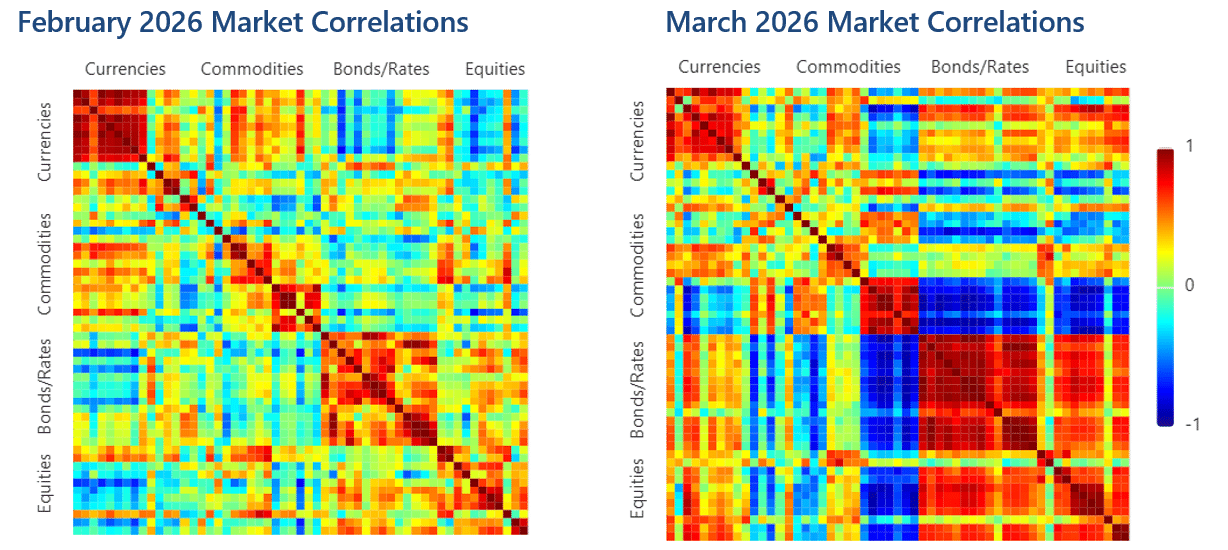

Correlations rose across and within asset classes. Treasuries once again didn’t behave like a hedge. Gold weakened alongside equities and bonds. The dollar strengthened as both a liquidity and yield vehicle. In short, this was a month in which the usual diversification architecture broke down at the same time the macro narrative itself was changing.

Cross-Asset Correlations: Energy Shock, Treasury and Gold Hedging Breakdown

Source: Graham Capital Management

The Fed’s Dilemma and the Macro Debate

The macro dispute in March was whether the front end of rates curves should move up to reflect renewed inflation risk, or down to reflect the growth destruction likely to follow from a severe energy shock. Markets initially chose the former. We still believe the near-term deeper macro logic favors growth damage over sustained inflation, especially if the shock persists. Large oil spikes tend to do more damage to GDP than they add to sustained inflation, particularly when central banks begin from a restrictive or even modestly restrictive stance. Graham’s economists made the same point differently: under extreme oil assumptions, the Fed’s own framework struggles to justify hikes and instead eventually points toward lower rates because the growth channel dominates. That does not mean markets cannot first trade the shock as inflationary. March showed that they can, and very violently. It does mean that the sequence matters: first inflation scare, then growth damage, then policy response.

Powell’s March press conference reinforced the dilemma. The Fed kept rates at 3.5% to 3.75%, described the current stance as within a plausible range of neutral, and acknowledged that events in the Middle East create uncertainty for the U.S. outlook. At the same time, Powell explicitly said the labor market has a “feel of downside risk,” even as he stressed the Fed is strongly committed to keeping inflation expectations anchored at 2%. That is the essence of the present bind. The Fed is not facing a clean demand slowdown that invites simple easing, nor an overheating labor market that demands hikes. It is facing a supply shock layered onto a labor market that is softer than headline resilience suggests. That is why the argument between the “hike because of oil” camp and the “cut because growth will crack” camp is so intense. Both see a real part of the picture. The first market move does not settle the macro debate.

The Fed Chair transition amplifies this uncertainty because the market can no longer assume a stable reaction function and must account for changes in the institution. Kevin Warsh was formally nominated, but his confirmation remains politically constrained by the Powell investigation and Senator Tillis’s stated opposition until that matter is resolved. The larger issue is not merely whether Warsh is “balance sheet hawkish” or “Fed funds dovish.” It is that he introduces new policy regime variables: less reliance on forward guidance, more willingness to challenge staff orthodoxy, more attention to the balance sheet and Treasury-Fed coordination, and therefore more uncertainty around term premium. The Fed Chair is powerful, but not omnipotent; the Chair’s power is ultimately the power of persuasion inside a committee. That suggests the transition may not produce an instant policy revolution. But it almost certainly produces more bond-market volatility, because the market must price both policy and a new institutional process at once.

This is also where the longer-term question of American exceptionalism starts to matter. We do not think the right way to frame this is “the dollar loses reserve status tomorrow.” Reserve-currency regimes do not collapse on cable television timescales. What changes first is the compensation investors demand for owning long-duration U.S. assets in a world where fiscal demands are rising, foreign-policy credibility is more openly questioned, and the relationship between Treasury and Fed independence is becoming a live political issue. The first manifestation of eroded confidence is not necessarily a weaker dollar every day. It is higher term premium, more fragile auctions, more appetite for gold and other neutral reserve assets, and a greater willingness by foreign investors to diversify marginal allocations away from U.S. duration. That is a slow-burn process, but wars, alliance strain, and institutional noise accelerate it. This process could accelerate further if foreign investors conclude that the administration is disregarding historical lessons about strategic overreach.

Q2 Scenario Analysis: A Narrow Base Case, A Wide Distribution

Scenario 1: Slower-Growth

Our base case for Q2 is not a clean soft landing and not an immediate recession. It is a slower-growth path in which the military situation does not meaningfully re-escalate, but energy and shipping conditions do not normalize quickly either. Under this outcome, Brent remains high through Q2, the risk premium fades only gradually, and the global economy absorbs a meaningful but not catastrophic terms-of-trade hit. For markets, that means the Fed stays on hold longer, while the back end of the Treasury curve must still price fiscal supply, institutional uncertainty, and the possibility that inflation settles above old comfort levels. Equities can rally episodically in this scenario, but leadership is unlikely to snap back cleanly to the previous large-cap duration complex. Energy, defense, selected industrials, and real-asset beneficiaries can continue to outperform, while higher-quality cyclicals and equal-weighted indices should fare better than the longest-duration growth segments if rates remain unstable.

Scenario 2: Persistent Choke-Point

The second scenario is persistent choke-point regime. Here, Iran retains de facto leverage over Hormuz through tolling, inspections, vessel vetting, or political bargaining, and traffic remains materially impaired. This is probably the most underappreciated path because it does not produce the drama of renewed kinetic strikes, yet it keeps the economic burden in place. In that world, the inflation data stay sticky for longer than central banks want, while real activity still erodes at the margin. Europe and Asia, as larger energy importers, would remain more exposed than the United States, reinforcing policy divergence and currency dispersion. Equities would likely become even more selective: import-heavy manufacturers, transport, chemicals, and low-end consumers would face pressure; energy, fertilizer, shipping, and defense would enjoy better earnings support; and global bond markets would continue to wrestle with the possibility that growth slows without delivering the kind of disinflation that gives policymakers comfort. That is a bad environment for passive beta and a better one for selective thematic and relative-value expressions across asset classes.

Scenario 3: Re-Escalation and Renewed Severe Hormuz Disruption

The third scenario is the most obvious tail: re-escalation and renewed severe Hormuz disruption. Here the temporary truce breaks down, shipping does not recover, and the world is forced to test the limits of emergency stock releases, demand destruction, and wartime policy intervention. The factual backdrop is sobering enough without embellishment. If this scenario reasserts itself, the first market move is directionally likely the same one we saw in March: front-end rates sell off on inflation fear, break-even inflation widens, equities de-risk, credit widens, and the dollar initially strengthens on liquidity demand. But if the disruption persists long enough, the path almost certainly becomes recessionary. At that stage, the market would transition from bear flattening to bull steepening as cuts are pulled forward at the front end while the long end remains less helpful because of term premium, supply, and governance risk. This is precisely why “bonds as a hedge” is no longer a one-line answer.

Scenario 4: Private-Credit Tightening, AI-Led Hiring Weakness, and a Capex Pause

The fourth and, in some ways, most important scenario is the one in which the geopolitical shock is merely the catalyst for a domestic U.S. rollover that was already latent given private-credit tightening, AI-led hiring weakness, and a capex pause. This is the path that makes us more skeptical on U.S. growth than we were at the start of the year. The IMF has flagged private credit as a rapidly growing asset class with meaningful vulnerabilities that now rivals major credit markets in size. Our concern is that BDCs and interval funds sit on liquidity mismatches that can export stress into public credit markets and ultimately bank balance sheets. At the same time, the labor market may be weaker than it looks, because AI is showing up first through vacancy destruction and slower white-collar hiring rather than through a classic layoff cycle. March payrolls were stronger at the headline level, but the number of long-term unemployed is up over the year and discouraged and marginally attached workers have risen. If war uncertainty then pushes CEOs to slow capex and hiring into the midterms, the policy conversation changes quickly from “higher for longer” to “how fast does the Fed have to go once the growth data crack?” though any easing cycle would likely proceed more cautiously if inflation remains elevated.

This domestic-rollover scenario is also the one in which the market may be most wrong on rates. If the growth hit comes through financial conditions, lending, and labor demand rather than primarily through energy price effects, the Fed may eventually cut later, but then more aggressively, than is currently priced, especially under a new Chair trying to establish credibility through responsiveness to deteriorating conditions rather than ideological purity. The long end may still discount deficits, Treasury supply, and a more politicized institutional framework. In that world, lower front-end yields would coexist with a less reliable rally in long Treasuries. Credit would suffer more clearly than rates at first. Equities would not necessarily be uniformly bearish, however. If lower rates arrive because capex and labor weaken, equal-weight, deep value, selected industrials, and policy-favored market segments could still outperform the most crowded duration-heavy leaders, particularly if the market also begins to discount a broader rotation away from the peak U.S. exceptionalism trade.

Taken together, these scenarios leave us more cautious on the U.S. growth outlook than we were three months ago. That does not mean that recession is the base case for Q2 itself. It means the balance of risks has shifted decisively toward a slower, more fragile U.S. economy in the second half of the year. The reason is not one variable; it is convergence. The war acts like a tax. Private credit tightens availability of capital. AI restrains hiring at the margin before it visibly boosts aggregate demand. Tariff headlines continue to widen the distribution around corporate planning. The midterm calendar sits in the background, shaping fiscal incentives and policy risk. Any one of these can be managed. Together, they create an environment in which even corporates that remain fundamentally healthy may choose to delay hiring, defer capex, and hold liquidity. That is enough to matter macroeconomically, though elevated inflation may complicate the Fed’s ability to respond quickly with easing.

Mapping the Scenarios Across Asset Classes

For fixed income, the durable message is less “buy duration” than “think in curves.” The front end is where slower growth eventually shows up; the long end is where term premia, Treasury supply, persistent inflation and institutional credibility are repriced. That could leave steepening as the more robust expression across scenarios with varying conviction across different markets, even if tactical rallies in duration occur on de-escalation headlines. Flexibility in positioning will be key.

For equities, the key point is breadth. This is less a blanket bearish call than a challenge to the narrow 2025 leadership structure: if rates stay unstable and capital discipline rises, broader value, industrial, and security-linked exposures could fare better than the most duration-sensitive winners of the last cycle.

For credit, the message is selectivity. Public spreads have not yet fully reflected the tighter conditions already emerging in private credit, which means apparent resilience should not be mistaken for safety.

For currencies, the dollar may still benefit in acute stress, but the medium-term backdrop is less one-sided as reserve diversification and institutional concerns build.

For commodities, energy remains the fulcrum. Gold may become a cleaner macro hedge again, while copper remains tactically more cyclical than its long-run scarcity story suggests.

What to Watch in Q2

The signposts for Q2 are now clearer:

First, watch actual Hormuz traffic and whether the ceasefire translates into physical reopening rather than diplomatic ambiguity, recognizing that any sustained disruption will be felt unevenly across regions and could drive greater cross-country divergence.

Second, watch whether Brent follows a normalization path or stays closer to the persistent-risk-premium world implied by a cold ceasefire.

Third, watch labor breadth, not just headline payrolls: quits, openings, participation, and long-term unemployment matter more than a single monthly payroll print.

Fourth, watch the private-credit complex for gates, forced sales, and signs that bank lending standards are tightening around it.

Fifth, watch the Warsh process not only for the nomination outcome, but for what it does to the market’s sense of Fed independence and Treasury-Fed coordination.

In 2026, the order of events matters at least as much as the outcome itself. That was true in January, and it is even more true now.

In conclusion for Q2, the late-2025/early-2026 U.S. upturn was real, but it has been interrupted by a geopolitical regime shift that turned into a much fatter-tailed distribution. The ceasefire lowers the immediate probability of the worst outcome, but it does not restore the old world. Markets are now pricing not just growth and inflation, but chokepoints, institutional credibility, and policy improvisation. That is why the right stance is more skeptical on U.S. growth, more respectful of tail risk, and more focused on sequencing than on single-point forecasts. The immediate lesson from March is humility. The strategic lesson for Q2 is that in a world of supply shocks, private-credit fragility, AI-led labor uncertainty, and Fed transition risk, flexibility and disciplined risk management matter more than elegant forecasts which currently have an even shorter half-life than normal.

Author Jens Foehrenbach President and CIO

Jens Foehrenbach, CFA, is the President and Chief Investment Officer of Graham Capital Management, L.P. (“Graham”). Mr. Foehrenbach oversees and supervises Graham’s discretionary and systematic portfolio manager teams, trading, and research. Mr. Foehrenbach is also a member of the firm’s Executive, Investment, and Risk committees. Prior to joining Graham, he worked at Man Group from September 2008 to February 2025, most recently as Head of Public Markets within Discretionary Investments at Man Group. Mr. Foehrenbach has served in several capacities for the Man Group during his tenure at the firm, including Chief Investment Officer of Man Solutions and Chief Investment Officer of Man FRM. Prior to joining Man Group, Mr. Foehrenbach worked at Harcourt Investment Consulting AG as Senior Analyst and Head of Relative Value. Prior to Harcourt Investment Consulting AG, he was employed by UBS AG, where he worked on the bank’s fixed income derivatives trading desk in Switzerland and London. Jens Foehrenbach received a Master’s degree in Business Economics from the University of Basel, Switzerland in 2001.

DISCOSURE

This presentation includes statements that may constitute forward-looking statements. These statements may be identified by words such as “expects,” “looks forward to,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “will,” “project” or words of similar meaning. In addition, our representatives may from time to time make oral forward-looking statements. Such statements are based on the current expectations and certain assumptions of Graham Capital Management’s (“Graham”) management, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Graham’s control, affect the operations, performance, business strategy and results of the accounts that it manages and could cause the actual results, performance, or achievements of such accounts to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical trends.

This document is not a private offering memorandum and does not constitute an offer to sell, nor is it a solicitation of an offer to buy, any security. The views expressed herein are exclusively those of the authors and do not necessarily represent the views of Graham Capital Management. The information contained herein is not intended to provide accounting, legal, or tax advice and should not be relied on for investment decision making.

Tables, charts, and commentary contained in this document have been prepared on a best-efforts basis by Graham using sources it believes to be reliable although it does not guarantee the accuracy of the information on account of possible errors or omissions in the constituent data or calculations. No part of this document may be divulged to any other person, distributed, resold and/or reproduced without the prior written permission of Graham.

Subscribe to our Resource Center

By clicking the Button you confirming that you’re agree with our following Terms and Conditions

By clicking register you are confirming that you agree with our following Terms and Conditions

Welcome to Graham Capital Management

By entering this website you are agreeing to its Terms of Use.

The risk of loss in trading commodities can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage that is often obtainable in commodity trading can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

In some cases, managed commodity accounts are subject to substantial charges for management and advisory fees. It may be necessary for those accounts that are subject to these charges to make substantial trading profits to avoid depletion or exhaustion of their assets. The disclosure document contains a complete description of the principal risk factors and each fee to be charged to your account by the commodity trading advisor (“CTA”). The regulations of the commodity futures trading commission (“CFTC”) require that prospective clients of a CTA receive a disclosure document when they are solicited to enter into an agreement whereby the CTA will direct or guide the client’s commodity interest trading and that certain risk factors be highlighted. This brief statement cannot disclose all of the risks and other significant aspects of the commodity markets. Therefore, eligible investors should carefully study the disclosure document to determine whether such trading is appropriate for you in light of your financial condition. Eligible investors are encouraged to access the disclosure document by contacting Graham, which will be provided at no additional cost. The CFTC has not passed upon the merits of participating in this trading program nor on the adequacy or accuracy of the disclosure document. Other disclosure statements are required to be provided to you before a commodity account may be opened for you. By accepting the terms of this statement and entering the site you are confirming your understanding of this statement.

Any “benefit plan investor” (e.g. An IRA or other ERISA investor) investor is hereby deemed to represent to Graham Capital Management (“Graham”) that an independent fiduciary (as defined in the ERISA fiduciary rule) is exercising its independent judgment with regard to such investor’s investment in any Graham managed fund and is aware of and acknowledges and agrees that Graham and its affiliates are relying on the exception set forth in clause (c)(1) of the ERISA fiduciary rule (i.e., the “transactions with independent fiduciaries with financial expertise” exception) with respect to any communications made to the investor or the investor’s fiduciary that are considered recommendations concerning any transaction and such benefit plan investor.

Although the site may include investment-related information, nothing on the site is a recommendation that you purchase, sell or hold any security or other investment, or that you pursue any investment style or strategy.

We do not give any advice or make any representations through the site as to whether any investment is suitable to you or will be profitable.

Nothing on the site is intended to be, and you should not consider anything on the site to be, investment, accounting, tax or legal advice. If you would like investment, accounting, tax or legal advice, you should consult with your own financial advisors, accountants or attorneys regarding your individual circumstances and needs.

The past performance of any investment, investment strategy or investment style is not indicative of future performance.

If you have been provided with a password to access the site you are solely responsible for maintaining the confidentiality and security of your password. You may not disclose your password to any third party. You accept full responsibility for any use of your password. You must notify Graham immediately of any actual or suspected loss, theft or unauthorized use of your password.

We are not obligated to inquire as to the authority or propriety of any use of or action taken under your password. We will not be responsible for any loss to you that arises from such use or action or from your failure to comply with these provisions.

The site, including all content, is provided as is and as available.

We disclaim all representations and warranties, express or implied, of any kind with respect to the site and the content including warranties of merchantability, fitness for a particular purpose and non-infringement of intellectual property and proprietary rights.

Without limiting our general disclaimer, we do not warrant the availability, accuracy, completeness, timeliness, functionality, reliability, sequencing or speed of delivery of the site or the content.